by

by When you are investing in a mutual fund, you are actually giving the investment money to the Asset Management Company, to invest on your behalf. They charge a fee for managing your asset which in financial terms is called “Expense Ratio”. Do you know a high expense ratio in a mutual fund can eat up your profits in the long run? Knowing how this thing works will help you to make an informed decision before selecting a Fund. Let us see how expense ratios in various situations can have different effects in your portfolio.

- What is the expense ratio?

- Why is the expense ratio deducted?

- When expense ratio is deducted and How it is calculated?

- Does the expense ratio have a Ceiling Limit?

- Can Mutual funds change expense ratio? If yes How often?

- Expense Ratio in SIP Vs Lump Sum

- Expense ratio in Positive and Negative returns, No returns

- Expense ratio in Active Mutual Funds – Direct Vs Regular Plans

- Expense Ratio in Passive Funds – Index and ETFs

- Why Does Expense Ratio Matters?

- Does Expense ratio include all Fees?

- Where to find the Expense Ratio of a fund?

- What Expense Ratio is too high or reasonable? How to decide?

- Conclusion

1) What is the Expense Ratio?

An Expense ratio also called as Management expense ratio (MER) or Total expense ratio (TER) can be defined as a measure which tells us how much the assets of the Fund is being used for administrative and other operative expenses. Expense ratio varies for different types of fund and is not a fixed value for all funds.

2) Why is the Expense Ratio deducted?

When you are giving your money for investment to a Fund management company, say for SBI mutual fund or HDFC Mutual Fund or any other Asset Management company (AMC), they will have a Fund Manager, who will invest your money in a basket of stocks and he will buy / sell the stocks on behalf of you. The AMC will have to pay management fees or investment advisory fees to the fund manager.

Also, other costs like

- Auditing fees to audit the funds,

- Transactional costs while buying and selling the stocks

- Legal fees

- Marketing fees to advertise their product to retail investors, sending mails, TV, Paper AD

All these costs will be deducted from the Fund assets, thereby reducing the asset value and reducing the returns to the investors.

3) When expense ratio is deducted and How it is calculated?

If you don’t like math you can just take a view of it and go to next section :

Expense ratio is calculated by the simple formula as follows:

Expense Ratio = Management fees / Total Assets of the fund

Let us understand with an example :

For example if the total asset Value of the fund is 100 Crores and The Management fees is 1 Crore, then the expense ratio is

1 Crore / 100 crore = 0.01

In percentage it comes as 1%. So the expense ratio is 1% per year

For investors the deducted expense ratio will be given in a statement every six months. However, this expense ratio is deducted every day. Let us see how :

If you invest 10,00,000 (10 Lakhs) in a mutual fund with an expense ratio of 1% then you will pay 10,000 as management fees to the fund company annually.

But this deduction does not happen yearly, It is deducted on a daily basis.

Daily deductible amount = Total Management fees / Number of trading days in a year

10,000 / 300 = 33 INR per day

However, you will not be seeing the deduction everyday, the value of the amount you see in your account is only after deduction. That is after you invested 10 Lakhs the next day if the fund increases by 1% then your Gross value will be 10 Lakhs + 1% (10000) that is 10,10,000. In that amount they will deduct 33 Rupees and the end value you will see in your account will be

(10,10,000 – 33) = 10,09,967

| Invested Amount By You | Annual Expense Ratio 1% | Daily Deduction | If fund gains 1% the nest day Gross value will be | Amount you will see in your account at the end of day will be |

| 10,00,000 | 10,000 | 10,000 / 300 = 33 | 10,10,000 | 10,09,967 |

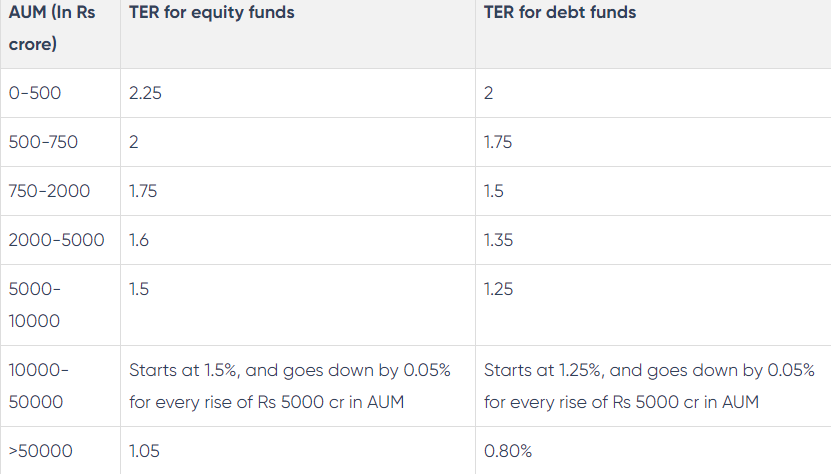

4) Does the expense ratio have the ceiling limit?

Even though the expense ratio can vary from one company to another, SEBI has made sure to protect the investor’s interest. Otherwise, the AMC can misuse your money for unnecessary advertising or paying huge money to fund managers like that. Below is a table that shows the Ceiling limits for different fund types.

5) Can Mutual funds change expense ratio? If yes How often?

Expense Ratio is not a fixed value. It can vary from time to time depending on the assets of the fund. Most fund houses when they start new offer low expense ratios to the customers, but once the customers join and the net asset increases they gradually increase their expense ratios. This sometimes can be more frustrating to an investor, especially if he/she has invested in the fund after so much research on their own.

Also, if the company spends more money on advertising or hires a new fund manager who may charge a little more than the old fund manager, the expenses for the AMC naturally goes up and it is the investors who have to bear the cost. In converse, if the fund house reduces the expenses then expense ratio will come down benefiting the retail investors.

As a general rule, if the fund asset increases to a greater extent, say above 55000 Crores or more the expense ratio usually goes down as the expense the company makes is distributed among a large number of investors.

6) Expense Ratio in SIP Vs Lump Sum :

Whether you are a lump sum investor or a Systematic investor the expense ratio will be the same for both. However, for a lump sum investor the deduction will be for the entire amount he invests in one shot, while for the SIP investor the deductions will be calculated periodically as he invests.

For example, if an SIP investor invests 10000 in a month Expense ratio will be calculated only for 10,000 in that month. When he invests another 10,000 in next month then expense ratio will be calculated for 20,000 (Including the last month investment) and so on.

7) Expense ratio in Positive and Negative returns, No returns :

This point is very important. Whether you are making positive returns in a year or negative returns or no returns at all your expense ratio will be reduced. That means, the AMC will be getting their expenses deducted from your investment irrespective of whether you make money or not. Let us understand by the following table in which the expense ratio is 1% and the amount invested is 10,00,000 –

| Amount Invested | 2% Positive return | No Return | 2% Negative Return |

| 10,00,000 | 10,20,000 | 10,00,00 | 9,80,000 |

| Deductible 1% | 10,000 | 10,000 | 10,000 |

| Amount You will see in your Account | (10,20,000 – 10,000) = 10,10,000 | 9,90,000 | 9,70,000 |

From the above table, it is very clear that irrespective of the returns you make, positive or negative, the expense ratio is constant and will be deducted from you.

8) Expense ratio in Active Mutual Funds – Direct Vs Regular Plans :

Active funds are managed by a fund manager who is actively involved in buying / selling a particular stock on behalf of you. Since, the fund manager should have more expertise in selecting a proper portfolio for you and to increase your returns thereby beating the index, he will be given more management fees and hence the expense ratio will also be higher.

Also, depending on whether your fund is direct (Investor directly invests with the AMC without any distributor to facilitate the transaction) or Regular (Investor invests through an intermediary, a distributor, broker or banker who is paid a distribution fee by the AMC) the expense ratio will vary.

Direct plans will be less costly when compared with the Regular plans since in Regular plans, the distribution fees paid by the AMC to your distributor will also be added to your expense ratio. So, always try to invest in a direct fund.

9) Expense Ratio in Passive Funds – Index and ETFs :

Passive funds are funds which invest money similar to that of Nifty constituents. They are generally called Index funds or ETFs (Exchange Traded Funds).

For example SBI Nifty Index fund- Direct invests in all the Nifty 50 stocks in the same composition as of nifty index. This has a very low expense ratio of 0.17% if the plan is direct and 0.49% in case of SBI Nifty Index fund- Regular plan. Note that, even in passive funds the expense ratio is higher in case of Regular Plan than Direct plan.

10) Why Does Expense Ratio Matters?

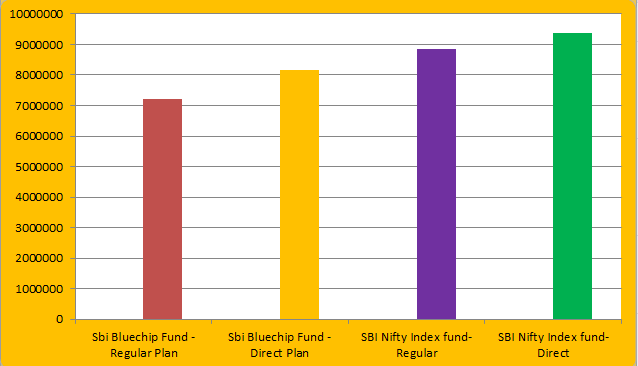

While it may be seen that the expense ratios as a ratio is very small like 0.4 -1% in the longer run it may have a huge impact on your returns. We will understand how a high expense ratio can affect your overall returns in a very long run with an example. Let us assume that you invest 10,00,000 in four different funds with four different expense ratios, for a period of twenty years with a CAGR of 12%

| Type of Fund | Amount Invested | Expense Ratio | CAGR % | Final Return Amount |

| Sbi Bluechip Fund – Regular Plan | 10,00,000 | 1.61% | 12 | 72,20,955 |

| Sbi Bluechip Fund – Direct Plan | 10,00,000 | 0.94% | 12 | 81,49,920 |

| SBI Nifty Index fund- Regular | 10,00,000 | 0.49% | 12 | 88,36,419 |

| SBI Nifty Index fund- Direct | 10,00,000 | 0.17% | 12 | 93,57,643 |

From the above chart you can see how a small variation in Expense ratio can affect the portfolio returns in the long run. So, it is always advisable to give importance to expense ratio.

11) Does Expense ratio include all Fees?

While expense ratio involves all the fees and expenses done by the AMC it does not include the exit loads. Exit loads are nothing but a penalty like fee that would be charged when you exit a mutual fund due to any reason within a year. Exit loads are not applicable for mutual funds you exit after a period of waiting period. This exit load is usually 1% of the invested amount. This 1% will be charged extra and will not be included in the expense ratio.

Also, any Long term capital gains (LTCG) or Short Term Capital gains (STCG) will not be included in this expense ratio.

12) Where to find the expense ratio of the mutual funds?

Though there are multiple websites that will give you the details of expense ratio the most commonly used sites are value research / money control. Just go to their site, search your favorite mutual fund scheme and you will know the expense ratio.

13) What Expense Ratio is too high or reasonable? How to decide?

As we have seen in the above examples, it is clear that we should go for direct funds instead of regular funds as it is very expensive. There is no confusion in it.

However, the confusion comes whether it is better to go for active funds or passive funds like index funds just for the sake of expense ratio.

Selecting a mutual fund, only based on expense ratio is never a good idea. The returns of the fund is more important than the expense ratio. Suppose, if the Active fund gives a CAGR return of 18% over a ten year period when compared to an Index fund with a CAGR return of 12%. Which fund will you choose? Just because the expense ratio in Index fund is lower will you forgo the extra 6% return offered by Active fund? No right? In this case, it is wise to choose an active fund over a passive fund.

But, unfortunately all the returns you see are of past history, and there is no guarantee that your active fund will beat the index in the coming years. Then, how to decide? Let me give you a suggestion which I feel will be useful to you. If you have some knowledge regarding investments or you can spend time to keep on learning about investments, then you can consider going for a good performing active fund. But, if you are someone who has no interest in this and you just want to do passive investing in equities then go for an Index Fund. However, discuss with your financial advisor before you put your hard earned money.

14) Conclusion:

Hope this article would have given an insight of how expense ratio is calculated and how you can make use of it in your investing journey. While expense ratio is an important thing to consider for long term investing, it is not the only thing you should be worried about. There are multiple factors you should take into consideration. Subscribe to our website to get the newsletters delivered to your mail, where I will be writing more about personal finance and investments strategies.

6 thoughts on “Expense Ratio in Mutual Funds- What? How? When? Why?- Everything you need to know”