by

by Bank fixed deposits is one of the easiest and common investing options available to the majority of retailers. The conception that the Bank FDs are very safe and guaranteed interest rates hook the retail investors to put their money with the banks. However, investing your money in Bank FDs will erode the value of your money over a long time. We will discuss here why and how the Bank FDs is not that much a good option when investing for a long time and the risk involved with Bank Fixed Deposits and how you can make an informed decision in your investing journey.

- Myth of safety

- Liquidity risk

- Taxation Risk

- Inflation risk

- Should I avoid Bank Fixed deposits altogether?

- How much money can I invest in Fixed deposits?

- What are other relatively safe alternatives to Bank Fixed deposits?

- Key Takeaways

Myth of safety:

Survey shows that a vast majority of people believe that the bank Fixed Deposits are very safe and there is no risk involved at all, and the bank is completely liable for their money in case of any defaults in the bank. But, as per RBI regulations investment amount up to 5 Lakhs only is guaranteed by Deposit Insurance and Credit Guarantee Corporation (DICGC).

In other words, suppose if you have made an investment of about 60 Lakhs in a Bank Fixed Deposit, you are guaranteed only 5 Lakhs of your entire investment in case of any bank defaults. There is no liability for the remaining 55 Lakhs. Even though such incidents are rare and usually the Government will come to rescue, the belief that the Bank deposits are completely risk free is a myth. Also, even though you may get the lost money in case of a bank default, nobody can tell you when you will get the money. It may be within a year or it may take even 10 years.

Liquidity Risk of Fixed Deposits:

The amount invested in Fixed Deposits are not accessible immediately. You have to apply for premature closure of your Fixed deposit in case you need money for an emergency. Even if you get the money within a couple of days, most banks levies a penalty by reducing the interest promised to you.

For example, in case of Fixed deposit by private finance companies (they give higher interest than the banks) you cannot close the Fixed deposit for the first three months. Your money will be locked for the first three months. In case you close the FD after 3 months but before 6 months no interest will be given and if you close the Fixed Deposit prematurely then there will be a reduction in the interest rate by 2%. So, if they had promised you an interest rate of 9% per annum you will receive only 7%.

Taxation risk of Fixed Deposits:

Any interest more than 10000 INR you receive in an academic year through Bank Fixed Deposits are taxable. (Interest earned upto 50000 are exempted from tax for senior citizens)

They are taxed depending on the tax slab you are in. Suppose you are in a 20% tax slab you will be taxed 20% on your interest. This affects the net interest rate considerably.

For example, let’s assume that you had earned an interest of 25000 in a financial year at an interest rate of 6%. The first 10000 is exempted from tax, so for the remaining 15000 interest earned you have to pay interest as per your tax slab. See the table below how the net interest rates differ after tax depending on the tax slab:

| Tax Slab in % | Interest amount before tax | Interest rate before tax in % | Interest rate after tax | Interest amount after tax |

| 10 | 15000 | 5 | 4.5 | 14925 |

| 20 | 15000 | 5 | 4 | 14850 |

| 30 | 15000 | 5 | 3.5 | 14775 |

So, if you are in the tax slab of 30% you just get 3.5% of interest in a financial year which is very similar to what you get in a savings account. You can argue that in small finance banks like Bajaj Finserv, ESAF gives an interest rate of 9% or more. It has its own risk and problems like defaults are not unlikely. Do your own research before investing in them.

Inflation Risk of Fixed Deposits:

When taxation risk reduces the value of the FDs in the long run, the most important but most neglected risk is the inflation risk. Many don’t consider the inflation risk while investing their surplus money in Banks. They are happy with the 5 -6% interest and think that their money is compounding year on year.

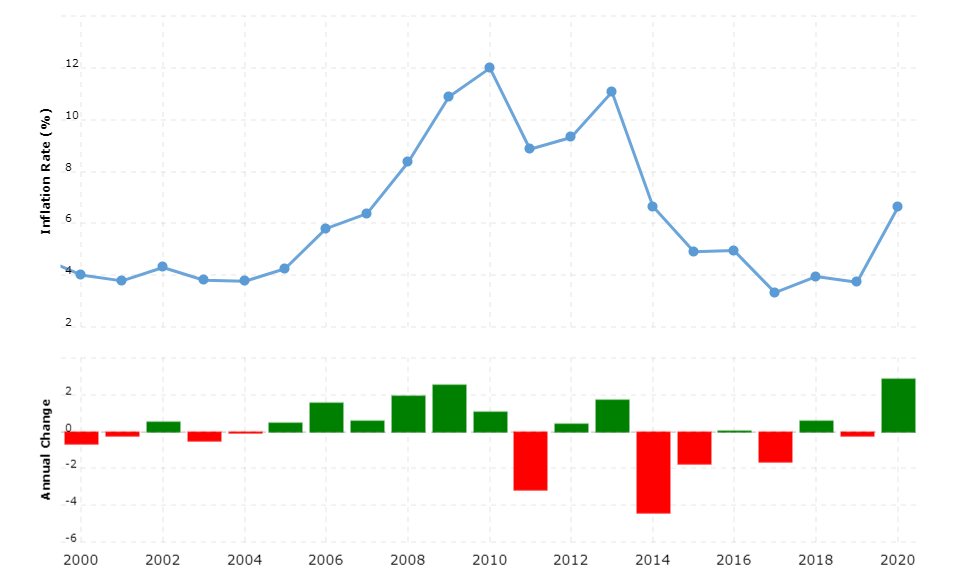

However, in reality money invested in Fixed deposits deteriorates and is surely a wealth destroyer. As per the report, it is said that the average inflation rate (inflation – rise of product prices, like commodities, food, hotels, education etc.,) in India for the past 20 years is around 7% (see the image below)

<a href=’https://www.macrotrends.net/countries/IND/india/inflation-rate-cpi‘>Source</a> Link source for image Inflation

So, with this inflation rate, the effective return you get by investing in Bank Fixed Deposits will be negative in a very long term.

The effective interest rate you will get is ( FD rate (-) Inflation rate )

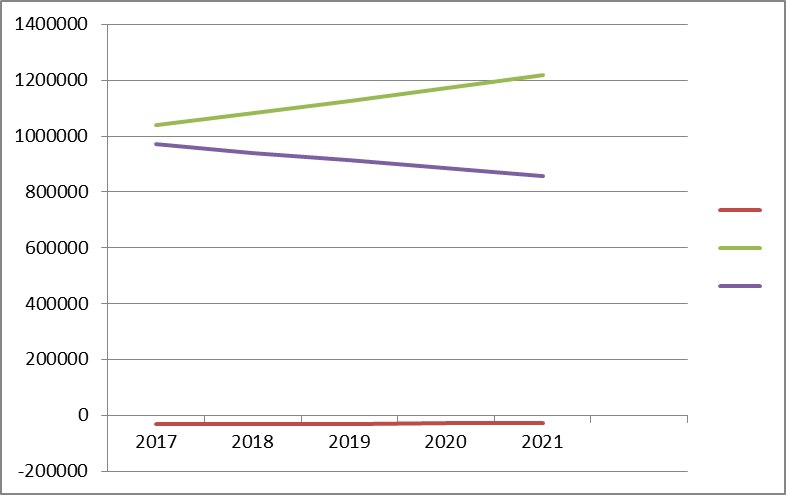

Lets see an example how your money will actually depreciate instead of appreciation over a period of time. For this let us assume that you are in a tax bracket of 20% and the FD rates given by your bank is 5% per annum. If the inflation rate is 7% then the

Effective interest rate = 4% – 7% that is -3%

It means that for the investment you make in FDs you would be making a value loss of 3% every year even though it seems that your investment is increasing.

| Year | Amount Invested | Amount with interest after tax ( 4%) | But actual value if adjusted to inflation 7% |

| 2016 | 1000000 | ||

| 2017 | 1040000 | 970000 | |

| 2018 | 1081600 | 940900 | |

| 2019 | 1124864 | 912673 | |

| 2020 | 1169859 | 885293 | |

| 2021 | 1216653 | 858734 |

While you think that your investments are increasing each year it is actually decreasing due to the effective interest rate when adjusted to inflation.

In the above chart the green line represents what you see in your bank account and the blue line represents what actually happens on a long run.

Of course, you may argue that not every year the prices are increasing, so this cannot be true. Yes, the prices don’t keep on increasing every year, it is different for different products. For example, school fees are not increased every year, but if it increases once in seven years the increase would be anywhere between 40-50% making an average of 7% per year. This is a compounded effect and not an every year event. In financial term it is called as CAGR.

Should I avoid Bank Fixed deposits altogether?

The examples we saw above are just to enlighten you about how only relying on Fixed Deposits may deteriorate our wealth in the long run. This does not mean you should stop investing in banks all together. Fds are a good option which are not affected by market fluctuations and the rule is you should know that more money in Bank FDs is not actually helping you to grow the money but to deteriorate it.

How much money can I invest in Fixed deposits?

While there is no general rule regarding the amount you should save in Fds. It is better to have at least 1 year of your annual expenses. For example, if you are spending 25000 per month then your annual expense is 25000 * 12 = 3 Lakhs. So, anything above than that is better to invest in equity markets / or other debt avenues.

What are other relatively safe alternatives to Bank Fixed deposits?

Debt Mutual Funds

Debt mutual funds invest in comparatively secured investment options such as corporate bonds, government securities and money market instruments. These are considered relatively safer than other mutual funds.Debt funds are capable of offering higher returns than fixed deposits. Also they have tax benefits like even if you are in 30% slab you need to pay only 20% if the holding period is more than three years.They are highly liquid and can be an excellent alternative to fixed deposits.

Liquid Funds

Liquid funds are a type of debt funds that invest only in high-rated money market instruments that mature within 91 days. The most important feature of liquid funds is that they provide liquidity. Therefore, apart from using liquid funds as an alternative for FDs it can also be used to park your emergency fund to help you at the time of crisis. The safety of the instrument is also high.

Equity Funds

These are a type of mutual funds that is usually managed by a portfolio manager. The manager buys commonly traded stocks as a basket and invests your money in that. In the long run equity mutual funds have proven to beat the index and are also safer than investing directly in stocks.

Corporate Fixed Deposits

If you are willing to take a little more risk, you can choose from corporate fixed deposit options which are nothing, but an FD offered by corporates. The advantage is that the interest rates offered will be higher than Fds. However there is always a risk of default. So it is important that you should research about the company wisely.

Government Bonds

In India, these are possibly the best and safest alternative to fixed deposits. The returns are only slightly higher than FDs, but it offers to diversify the portfolio. Also you can invest in debt mutual funds which only invest in Government bonds and securities. To know more about the debt funds visit sites like money control, value research etc.,

Key Takeaways

Though Fixed deposits are a well known savings option, with the interest rates falling to new lows each year, considering Bank Fixed deposits as an investment option does not hold good. It’s a sure way to deplete your wealth in the long term.

If you are investing in Fds more than the emergency corpus (varies for person to person) it’s high time you consider other alternatives as mentioned above.

One should remember that saving money and investing money are two different ball games. In investing you should be more clear where you are investing and how much you are investing in different asset classes.

5 thoughts on “Bank Fixed Deposits a definite wealth destroyer !!! Things you should know before investing in Fixed deposits”