by

by Life insurance is one of the most useful financial tools that everyone should have. It is a contract between an insurance company and an individual, where the company agrees to pay a sum of money to the individual’s beneficiaries in the event of the individual’s death. The insurance company pays the sum of money to the beneficiaries in exchange for periodic payments, called premiums.

Most people choose to buy life insurance for the peace of mind it provides. It is a way to financially protect your loved ones in case of your death. If you are the primary breadwinner in your family, life insurance can ensure that your loved ones will be taken care of financially in your absence. However, with multiple life insurance plans and many misleading advertisements by the marketing companies confuses a normal person which one to choose among the products available.

In this article, let us see what are the things to consider before buying life / term insurance. This article is deliberately written on getting pure term insurance instead of selecting a plan with maturity benefits or investment benefits. Keeping it simple and focusing on our key requirements when choosing a life insurance are discussed. Be sure that you read with focus as the points discussed here may require your keen attention.

When to buy insurance?

When it comes to buying insurance, your goal should be to get as much coverage as possible in exchange for the lowest premium. The best time to buy insurance is when you are young and healthy because the less your age, the lesser the premium amount you have to pay.

In simple words, the best time to buy insurance is as early in life as soon as you start earning. The younger you are, the lower your insurance premium will be. This is because insurance companies charge higher premiums to policyholders who are older and have health complications. So, always start early.

Always choose term insurance without any maturity benefits:

When buying life insurance be sure that you buy it only for the purpose of any untoward event. Don’t think of buying a life insurance which gives you premium amounts at the time of maturity say after thirty years. Selecting a pure term insurance with no maturity benefits will reduce your yearly premiums significantly and you can use that amount to invest in something else.

We all have car insurance. Do we think to get the premiums back? No right? We pay the premium just for that year and we forget about that. We claim it or not does not matter. One should come out of the mindset of getting the money back. Let me show you an example how selecting a plain Term insurance will reduce the premiums to a greater extent.

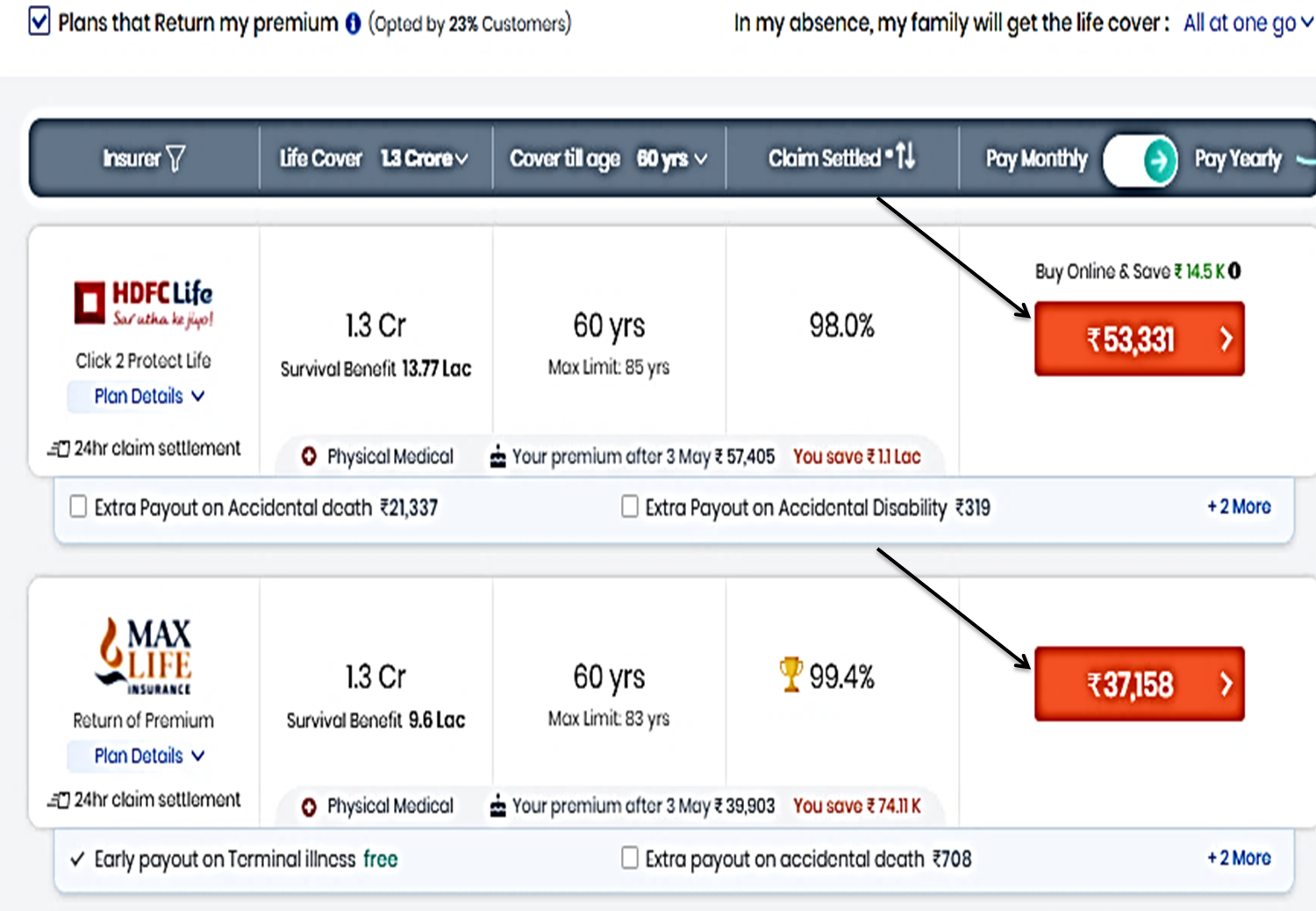

Below is the screenshot taken from Policybazaar website. Showing the premium for a term insurance for an individual at the age of 34 up to the age 60 for 1.3 Crores, without any money back policy. The premium comes around 18000- 19000 per year approximately.

Now, when a life insurance is selected with the option of returning your premium you can see that the premium goes to anywhere between 37000- 53000. You can see that even though the amount insured and the age of the individual at the time of taking the policy, the term of the policy (60 years of age) all remains the same, the premium is drastically high, when compared to a plain insurance.

How much to get covered?

This is the most important factor to consider when buying life insurance. Most people think that 1 crore is the highest cover one should aim for. But it is actually not true for each individual. It all depends on how much you spend for your family every year. You should always get covered for at least 20 times your annual expenses. This will ensure that your loved ones are taken care of financially in the event of your death.

This means that if you have an annual expense of ₹6,00,000, you should get life insurance coverage for at least ₹1,20,00,000. But imagine if the annual expense of someone is more than 12 Lakhs, then will the 1 crore coverage be enough? Definitely, no. They should at least get covered for 20* 12 Lakhs – 2,40,00,000 INR. Similarly a person with very little annual expense, say just 20,000 per month that is 2,40,000 per year need not go for a 1 Crore insurance, thereby saving the premium amount. Lesser the cover you ask for and lesser the term you ask for lesser will be the premium.

How long should I get covered?

We have seen above that selecting life insurance for a particular term is a better option. But how will you define that term? Is it 15 years / 20 years / 30? Which is good and sufficient? The answer to this question depends on your age and the amount of coverage you need.

Most people think that they can take life insurance till 99 years for 1 crore so that even if they die at 99th year their family will have a lump sum of 1 crore to live with. But they forget about the inflation factor. The value of money decreases over time, which means that the coverage you have today will be worthless in the future.

For example, let’s say you have a life insurance policy with a death benefit of ₹1 crore. The ₹1 crore can lose its value and become a lot less in the next 30 years due to inflation. It might only be worth ₹1-2 lakhs of today’s value or even less in the future. Inflation is a great factor when it comes to financial planning and that is why it is recommended not to keep a large amount of money in a bank account as it will be a wealth destroyer in the long run.

In my opinion, it is good to get covered till the age you want to work, or a maximum of five years more than that. Say, if you are 30 year old now and want to retire at the age of 55 then it is more than enough to get covered for 25 years or maximum 30 years. Because, as your age increases your liabilities should have come down and you should have already saved a good corpus for your retirement.

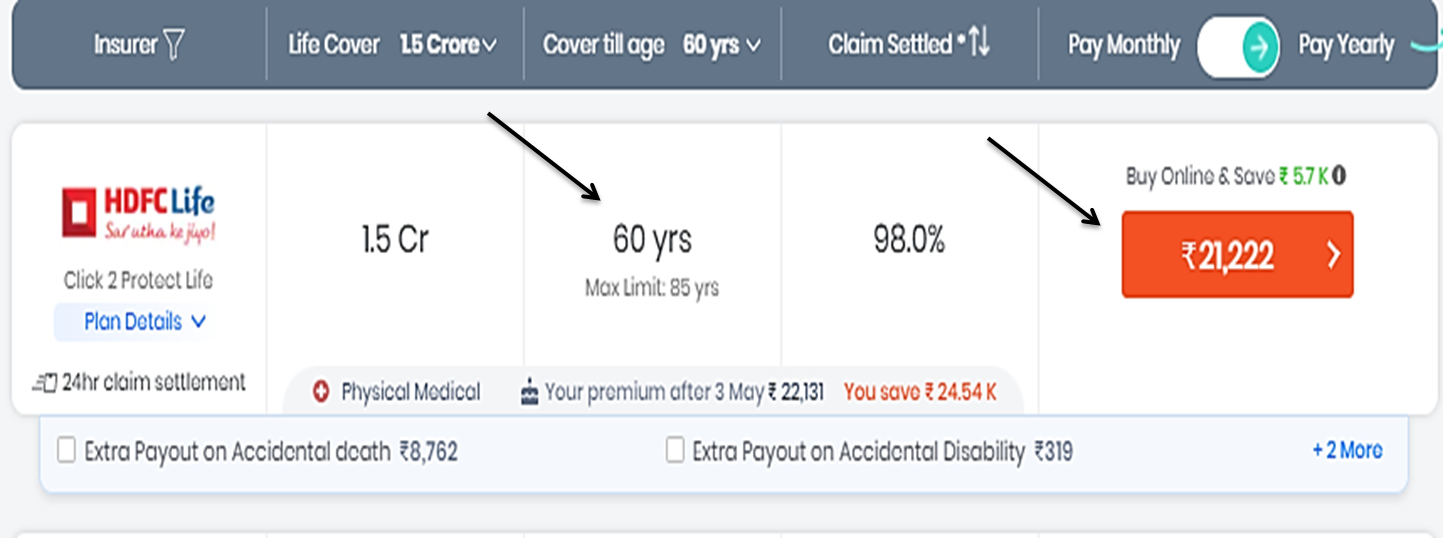

The liability you have at the age of 40 will not be the same as in your 50’s and even less in your 60’s. Your son / daughter would have finished their education and would be standing on their own. So, taking life insurance up to 80 years / 90 years does not seem to be valid in my opinion. Instead you can reduce the number of years you want to be covered and increase the amount of coverage you need. Instead of getting 1 crore coverage for 30 years, go for 1.5 crore coverage for 25 years or so.

Below is an example of how you can select a policy with the same premium amount by reducing the term of your insurance. In the image below you can see that the premium for a coverage of 1.5 Crores up to your 60th age is 21,222 INR.

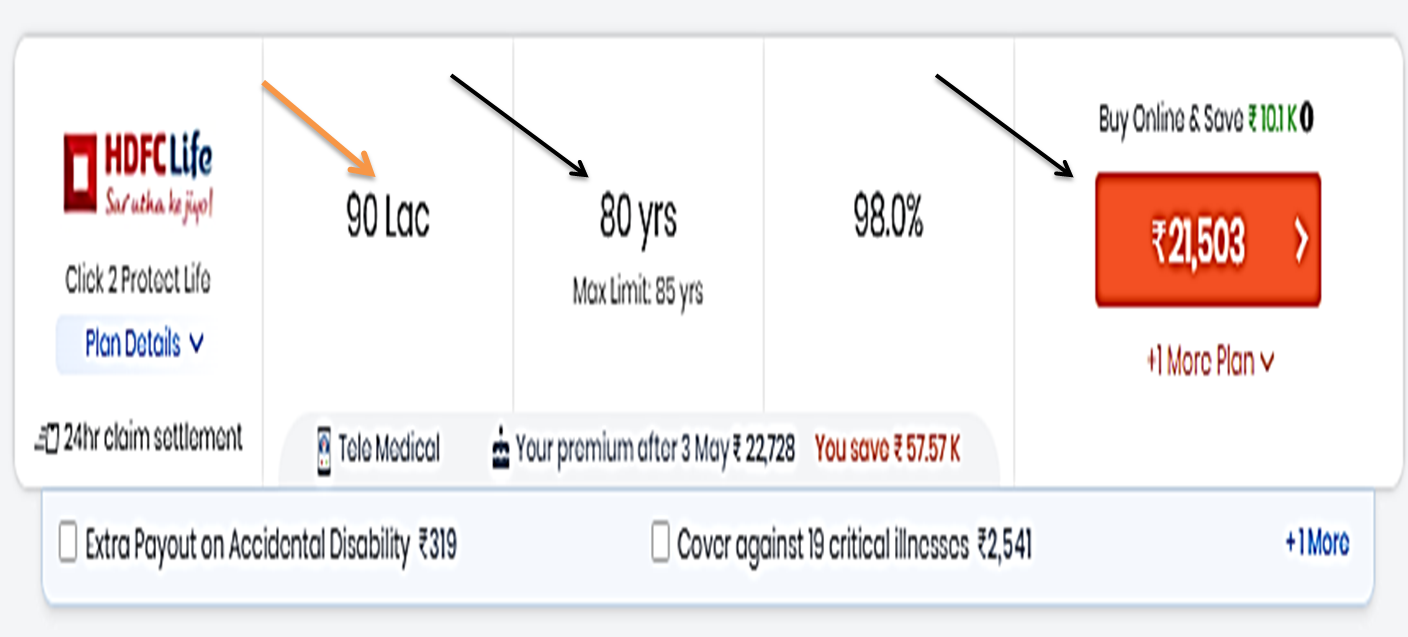

However, if you want a life insurance with the same premium and you want to get covered for up to 80 years instead of 60 years then you will be covered only for 90 Lakhs. If you want to increase the insured amount then you will have to pay a higher premium. See the image below :

How should I pay the premium?

Premium payment tenure is very important. Some companies provide you the following options:

- Monthly / Yearly Payment

- Pre pay

- Chunk payments like pay in ten years and get 20% off like that

Always choose the first option. This is because time is money. You should use it to your advantage. When you have the option of paying every year, why would you want to pay for the entire term (20/ 30 years) in one shot or in shorter periods of time like ten years? What if something happens to the insured in his/her second year of term period and he /she has already paid the entire amount for thirty years?

So, always pay every year instead of other options. One best way to pay the premium is by starting an RD every month and at the time of maturity, paying the premium. You can use this for any type of recurring expenses.

Settlement / Payout options:

Insurance companies give you four options of how your family will be paid the assured sum in case of any untoward event to the insurer. They are:

- Full payout as a lump sum – Entire amount is settled in one shot

- Regular income payout option – The insured amount is given every month like a salary till the amount lasts

- Increasing income Payouts – The insured amount is given every month / year with increasing option every year, thereby adjusting with the inflation

- Partial Payout and Partial payment – 50% Of amount insured is given immediately after the incident and remaining in regular intervals

In my opinion the regular income option is the worst as it does not consider inflation and your family will find it harder to manage with it as the time goes by. Even other options like increasing income and partial payout plus partial income may look attractive, but It is wise to get the money in one shot as Full payout. By this, your family will have full control over the amount and are not dependent on the insurance company anymore.

Claim settlement ratio is important but it does not guarantee you anything:

The claim settlement ratio is the percentage of total death claims that an insurer has paid in a financial year.

However, it is important to understand that the claim settlement ratio is not a guarantee that the insurer will settle your claim. Just because a company has a settlement ratio of 95% does not mean that your claim will be settled for sure. Each case is different and the insurer will take into account many factors before settling a claim

Some of these factors include

- The cause of death

- The rider benefits

- The terms and conditions

- The medical history of the policyholder and more

Thus, it is important to understand that the claim settlement ratio is not a guarantee that the insurer will settle your claim, and don’t select a policy just because the settlement ratio is good this year. There is no guarantee that the settlement ratio will be higher next year also. Just use this as an assessment tool and not a decisive tool.

How to choose a company?

Another question that pops into everyone’s mind is which company should I choose? Before choosing an insurance company you have to give utmost importance to the quality of the company. How long has the company been there and how big is it, should be the questions you should look for. Whether the insurance provider will be there after 30-40 years from today and be able to pay my family the insured amount without any delays or difficulty?

In India companies like HDFC, SBI, LIC, etc are too big to fail so you can choose any of them. Among these, you can choose the one with a lesser premium. Don’t choose a company that is relatively new and doesn’t have a track record for at least 10-20 years. You can consult your financial advisor if you are not sure what to choose. Don’t shy away from consulting a financial advisor.

Avoid riders (like Critical illness / Personal Accident etc.,) with Life insurance:

When you are buying life insurance, you will be offered many riders. Some of these riders can be useful while others are not.

For example, the critical illness rider pays out a lump sum benefit if the policyholder is diagnosed with a critical illness like cancer. The personal accident rider is a rider that pays out a lump sum benefit if the policyholder is involved in an accident.

These riders are not necessary when you already have life insurance and they increase the premium by a lot. Avoid these riders and just stick with plain life insurance. This will make it cheaper for you in the long run. If you still want to have the benefits of these rides take separate insurance for critical illness in the form of a powerful health insurance or personal accident policy. This will help you to get covered adequately.

Don’t mix insurance with Investments

Investments are meant to grow your money while insurance is meant to protect your family in case something happens to you. Simply put, insurance is a protection and investment products are wealth building tools. There are a lot of life insurance products available in the market which claim that you can have life insurance and build your wealth at the same time with the premiums you pay. They charge a hefty premium for these things.

These products are usually of two types:

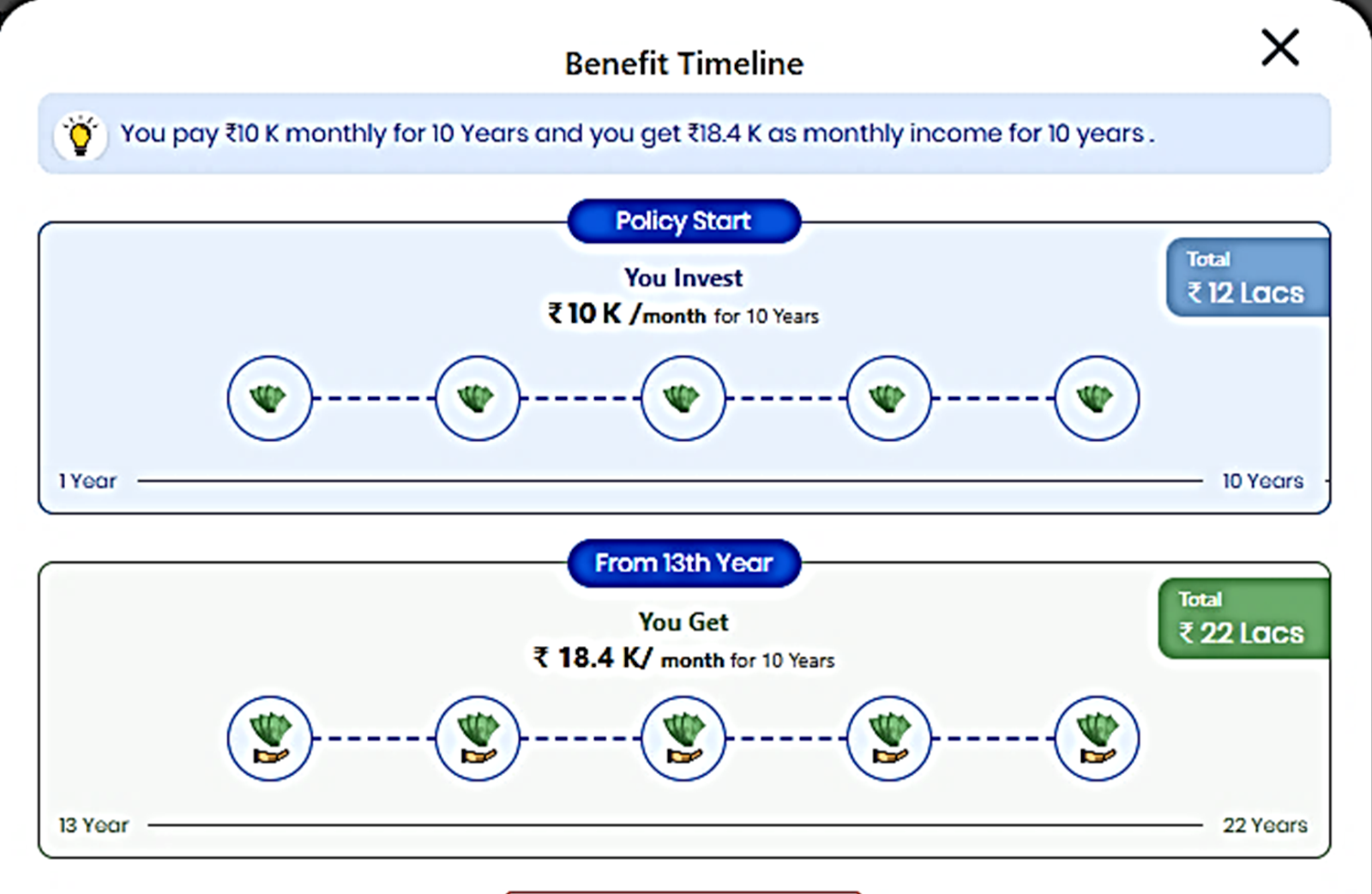

One is called as 100% guaranteed return scheme- In this you pay a premium for the first ten years and you get back the money in double from the eleventh year onwards for the next ten years. These plans will be like the image seen below:

In the image you can see that if you pay 10000 per month for the first ten years, then from the eleventh year you will be paid 18400 per month for the next ten years. So, you invest 12 Lakhs and get 22 Lakhs in return. Initially you may think “WOW!! We are getting double the money”. First understand that they are not giving you the money as a lump sum in the eleventh year. They will pay 18400 every month in installments for the next ten years.

Time is money and the money you get at the end of 20 years will be very less than if you had invested in mutual funds. So these 100% guaranteed return life insurance products are a waste of money in my opinion. Also, the amount you get covered for these entire 22 year is just 12 Lakhs (in the above example image). Think how vulnerable your family will be if something happens.

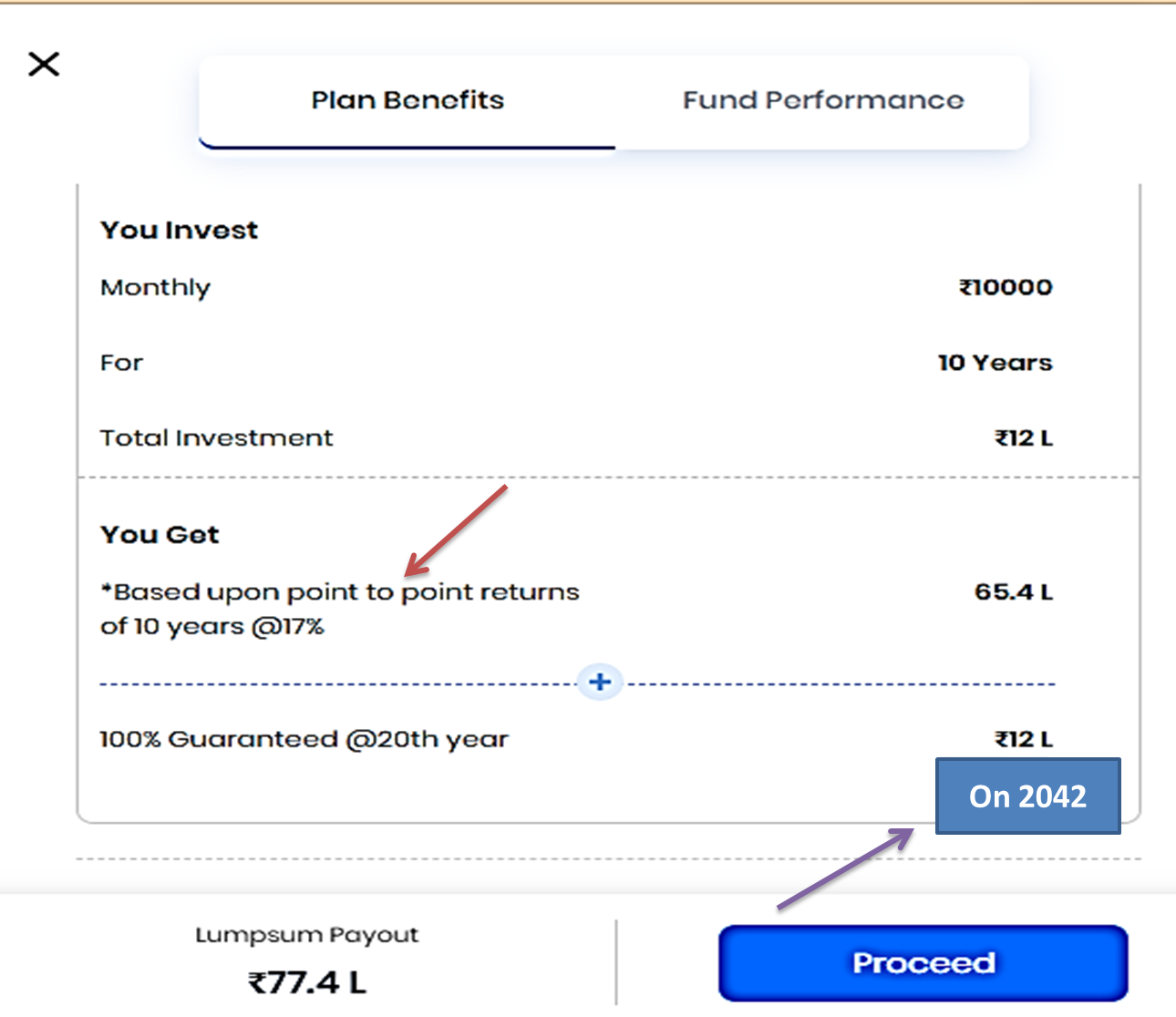

Second type of return oriented life insurance product is, you pay a premium and from that a portion will be taken for life insurance and remaining amount will go for market linked mutual funds. This is called ULIP plans – Unit Linked Insurance Policy.

In the sample picture shown above, you can see that you have to invest 10000 INR every month for ten years. At the end of the next ten years (Total 20 years) you will get the invested 12 Lakhs plus market return of 65.4 Lakhs. You may think that you are getting a good return with insurance also. But two things should be noted here:

- One is the return shown here is a point to point return (red arrow) based on past history. It shows a very attractive CAGR of 17% per annum. However, the past history is not a guarantee of future return. Also, investing based on seeing only the CAGR Returns may be misleading many times.

- Second is, you get covered only for 12 Lakhs (built in cover) during this entire 20 years, which in my opinion is nothing short of disastrous.

So, kindly stay away from these types of investment related life insurance schemes as they will do more harm than you ever think. You will be both under covered and under invested.

Take insurance with MWPA:

And lastly, always take insurance with the Married Women’s Property Act (MWPA).

The MWPA is a law that protects the property of married women from their husband’s creditors. This means that if you have any debts, the creditors cannot come after your family for the insurance money in case of any untoward event and your family will be safe.

Conclusion

So there you have it! Now you know the ten must-know things before you choose a life insurance policy. I had tried my best to make you understand what to look for and what to avoid while buying a life insurance. By following these tips, you will be able to make an informed decision and choose the right policy for you and your family. Always remember that life insurance is a safety measure and should not be seen as an investment option. Because at the end of the day, it is your family that is important and you want to make sure that they are taken care of. Have a happy and safe life!

2 thoughts on “Life Insurance – How to buy a Life Insurance? (Must know things before you choose one)”