by

by Do you know that according to a recent research only 44% of the Indian population is covered by Health Insurance. A vast majority of the population are not covered by health Insurance. If you are one, who is looking to take health insurance and is confused about how to decide on a good insurance policy, this article is for you. This article will discuss the must know facts you should consider before you buy a policy. By the end of this article, you will know exactly what to look for in a health insurance policy and take an informed decision.

- What is Health Insurance and Why is it important?

- When to take health Insurance?

- How much should I be covered?

- What Health Insurance type to take for my family?

- How to increase my Health Insurance cover?

- When Health Insurance can be claimed?

- Room Rent Sub limits in health Insurance

- Deductible Vs Aggregate deductible in Health Insurance

- Claim Settlement Ratio

- Co payment in health Insurance

- Waiting periods / Exclusions – In your Health Insurance Policy

- Can Health Insurance be ported to other companies?

- Points to keep in mind

- Key Takeaways

1) What is Health Insurance and Why is it important?

Health Insurance also called as medical insurance is a contract made between you and your insurance provider, by paying a premium to help you meet the medical expenses in case of any untoward events. The medical expenses are increasing day by day and the country is also growing fast. Increased health awareness among the public and the need to get world class treatment in a good hospital with better infrastructure contribute to the rise of medical expenses.

With inflation and other issues these expenses are only going to increase ever and there is no turning back. Getting treated in private hospitals with global standards can be very expensive and within a few days it may eat up your many years of savings in case of an accident or untoward health conditions. If you are in the beginning stage of your financial journey it may create a huge dent in your process. Sometimes, it can even shatter your dream of achieving financial freedom early. So, there is no question of asking whether one should take health insurance or not.

2) When to take Health Insurance?

Taking health insurance is something which you should do, even before you plan for your financial independence or investing your money in any other long term asset. Getting you and your family covered for health and life is the foremost thing you should do. So, you should take health insurance as soon as you get your job, or at least once you get married you should be having your insurance.

Health insurance if taken earlier has its own benefits. You will be healthier in your young age without any lifestyle diseases like high cholesterol, diabetes, heart issues etc., Most health insurance providers don’t even ask for a health check up if taken before 35 years of age. Another interesting benefit is the premium which will be much cheaper and you can get covered for a high amount also.

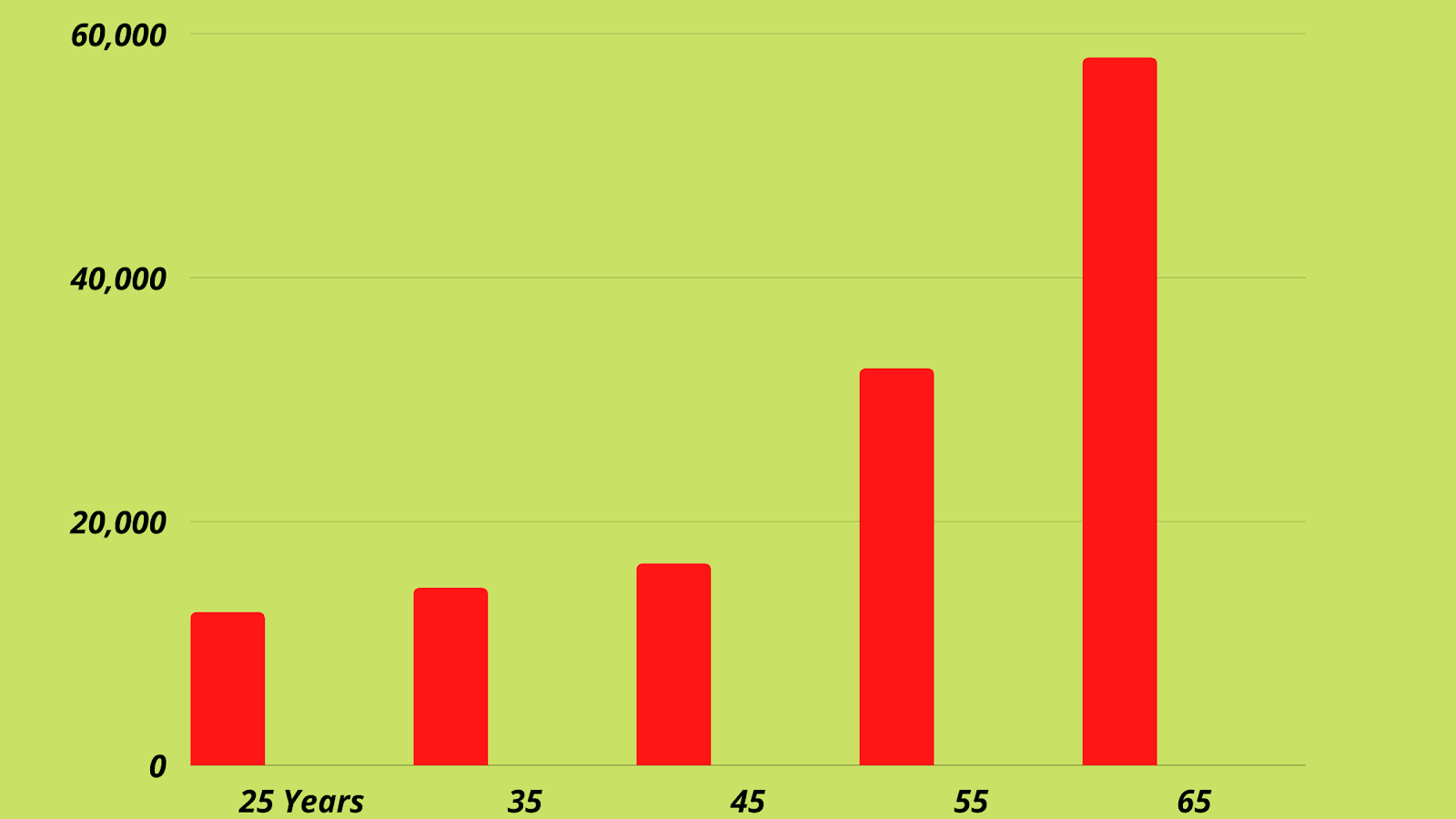

Let us see how the premium varies for a health insurance plan (HDFC Ergo optima Secure) as the age increases:

| Age of the Member insured | Sum Insured | Premium |

| 25 | 10 Lakhs | 12,500 |

| 35 | 10 Lakhs | 14,500 |

| 45 | 10 Lakhs | 16,500 |

| 55 | 10 Lakhs | 32,500 |

| 65 | 10 Lakhs | 58,000 |

So, opting for the health insurance in the early stage of life helps to reduce the premiums to a greater extent.

3) How much should my health insurance cover?

Though it may vary for different individuals depending on their income stream and needs, it is good to get covered for at least 25 Lakhs to 30 Lakhs. You may think that this is too much. Yes, as of now it is too much. But, think long term. After 10-15 years this amount will be just sufficient and not too much. This is due to inflation and increasing medical costs day by day, which will directly impact on the medical expenses you have to bear.

If the amount you need to shell out for a medical treatment in a good hospital with global standards is 5L today it will be 10-12 Lakhs in ten years. Remember, that most insurance companies do not allow the insured to increase the insured amount after a certain age period. So, it is better to get covered for a good amount today than trying to increase it at the time of need.

4) What Health Insurance should I take for my family?

The health insurance policy is mostly of two types:

- Individual Policy

- Family Floater Policy

Individual Policy:

In this, the sum is insured separately for each individual. For example, if the family consists of three members and each member is insured for three lakhs. So, in this case all the three policies are independent.

The disadvantage of this individual policy is that it cannot be transferred between individuals. For example if Person A is met with an accident and the total bill amount is four Lakhs, he will be paid three lakhs by the insurer, the remaining 1 Lakh should be borne by the insured. In case if the same person makes another claim of 1 Lakh in the later part of the insured year, he will get nothing since the entire insured amount of 3 Lakhs is exhausted.

Family Floater Policy:

This insurance floats between the family members. Suppose, in a family floater if the sum insured is for 5 Lakhs it can be utilized between family members. In the same example as stated above, Person “A” with this family floater will get the entire bill amount of four lakhs in his first claim and also the 1 Lakh for the second claim, as the total sum insured in for 5 Lakhs and is not exhausted by other family members.

So, what to choose? If you are taking health insurance in your young age, say below 35 years and your family members included in the family floater policy is also below 35 years, then the chances of all the members getting ill at the same time is very rare. In that case, it is always better to go for a family floater as the premiums will be significantly lesser than the individual policy. However, make sure that you don’t include your parents in this policy as the premiums are calculated based on the member who is aged most. So, if your parents are included in this, the premiums will be more. It is always better to take separate insurance for the senior citizens.

5) How to increase my sum insured after taking a policy?

Most of the people, after taking the insurance policy, feel that the sum insured is very less. When you take a family floater insurance with base cover of 5 Lakhs for three people (Parents and 1 Child) the premium usually comes to 15000 /- But, as seen above it is better to increase the sum insured to 25-30 Lakhs. However, the premium will go very high if you take a base cover for 25 Lakhs, which may come anywhere near 30,000 /-

Super Top Up Policy:

Here, come the Super Top Up policy for our rescue. This is nothing but an additional policy, which increases the sum insured, with lower premiums. For a sum insured of 20 Lakhs the premium comes upto 3000 per year. Suppose, in addition to the base cover of 5 Lakhs if you take this policy, you will be covered for additional 20 Lakhs thereby making the total sum insured to 25 Lakhs. The premium is also much lower (15000 for base + 3000 for Super Top up = 18000 /- Only per year)

Super top up comes into effect only when the base cover amount of 5 Lakhs is claimed in an insured year. This is called deductible. Let us see how this super top up works with an example:

Always buy a super top up policy with the same insurer as your base policy. Beware of Top Up policies which are different from super top up policy. Top up policies may require deductibles every time and will not come into effect immediately when your base cover is over. Threshold limit is applicable each time and is not cumulative as in super top up policies.

6) When Health Insurance can be claimed?

Health Insurance can be claimed either during the treatment as cashless method or after your treatment is over in reimbursement method.

In the Cashless method, you have to get admitted in the hospital which is a network of your insurer. The network hospitals can be seen in the policy issuer’s website. It’s always better to take note of these network hospitals so that in case of emergency you need not research on these hospitals at that time. Once you reach the network hospital, inform the billing section of the hospital regarding cashless treatment and show your insurance details. They will then inform the insurer and get approval for you. You can get treated without paying as per your policy allowances.

If you get treated in a hospital which does not come under their network hospitals, you can get treated first and then after your discharge you can apply with the insurer for reimbursement with relevant documents. Only thing is, you have to first pay from your pocket and then get reimbursed from the policy issuer.

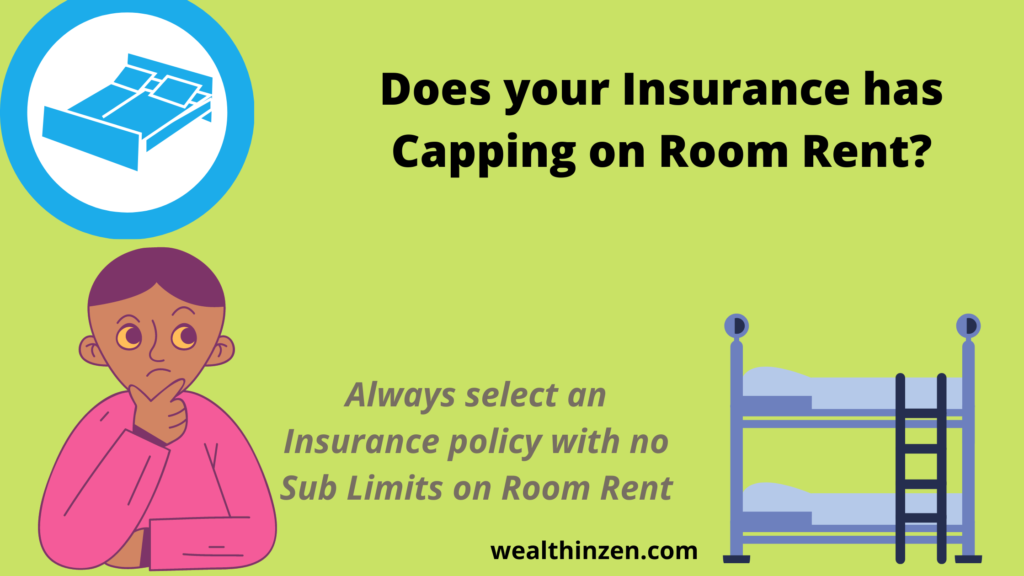

7) Room rent Sub-limits in Health Insurance:

One of the most important things to be considered in selecting a health insurance is room rent sub limits. Most of the policies issued by PSU companies will have a sub limit on room rent. Their policies will have a clause that will restrict the maximum room rent limit that you can avail to 1% of your sum insured . So, if you are insured for 4 Lakhs it means that you are eligible to get admitted in a room with a limit of 1% that is 4000 per day. Anything more than that will be a violation of the policy which will impact your claim.

You may think that this is not a great thing to worry about. Even if you take a room rent of 8000 per day for a total of 5 days, an extra 4000 per day, so a total of 20000 for 5 days can be easily managed by you. But, the catch is hospitals charge differently for the same procedure depending on the type of room you select.

An angioplasty done in a Deluxe suite room will be higher than when done in an AC single room. So, the insurer will pay you in proportionate to the sum insured.

So, if you take a room rent of 8000 per day instead of your eligible 4000 you will be paid proportionately only, as shown in the table below:

| Actual Bill | Reimbursed amount | Reason | |

| Room rent charges For five days at 8000 per day | 40000 | 20000 | Eligible for 4000 per day only |

| Surgery cost | 200000 | 100000 | Proportionate to room rent limit |

| Doctor’s fee and Investigations, tests | 25,000 | 12,500 | Proportionate to room rent limit |

| Medicines | 15,000 | 15,000 | At MRP as in Bill |

| Total | 2,80,000 | 1,47,500 |

So, in the above example the total amount to be paid from the pocket is 1,32,500.

Therefore, always select a policy which has no sub limits on room rent. Most of the private companies nowadays offer Single AC rooms with no sub limits, some expensive policies also allow deluxe rooms without any limits on room rent.

8) Deductible Vs Aggregate deductible in Health Insurance:

Deductible is nothing but an amount the policyholder is liable to pay before the insurance company starts paying. In other words, the insurance company will pay the amount only if the deductible amount is exceeded. If you have taken a health insurance policy with a deductible of 1 Lakh, it means that for any claim less than 1 Lakh has to be paid by the policyholder itself. The company will not pay anything. Only, if this 1 Lakh is exceeded the company will pay.

Always, it’s better to choose a policy with minimum or no deductibles. Higher the deductible amount lower will be the premium amount. So, many policyholders without knowing the catch will accept lower premium policies with more deductibles.

Also, always choose a policy with aggregate deductible. Aggregate deductible includes the amount paid by you in previous claims in a policy year while plain deductible policies do not consider the amount paid by you previously in the same policy year. Let us understand with the following example. Imagine, Person A has taken a policy for 5 Lakhs with 1 Lakh deductible, and Person B has taken a policy for 5 Lakhs with 1 Lakh aggregate deductible. Both makes three claims a year and this is how the policy works:

| Claims made | Claim amount | Person A – Deductible Plan (1 Lakh) | Person B – Aggregate Deductible plan (1 Lakh) |

| First Claim in January | 45,000 | Not exceeded 1 Lakh- so insurance company won’t pay any | Not exceeded 1 Lakh- so insurance company won’t pay any |

| 2nd claim in June | 2,00,000 | Exceeded 1 Lakh – Policyholder will pay 1 Lakh, Insurance company will pay 1 Lakh | Last time payment 45,000 will be considered. So, policyholder will pay only 55,000 (1 L – 45000) and insurance company will pay 1,45,000 |

| 3rd Claim in November | 50,000 | Not exceed 1 Lakh- so the insurance company won’t pay any. Policyholder should bear the entire cost | Insurance company will pay entire 50,000 as the policy holder has paid 1 Lakh in the previous two claims |

So, whenever you select a policy, make sure whether deductible is aggregate. Better to choose a policy with no deductibles.

9) Claim settlement ratio:

Claim settlement ratio measures the ability of the insurance provider to settle the claims. It is the number of claims settled against the total number of claims filed in a financial year. Suppose if a company has a claim settlement ratio of 96% it means that it has settled 96 claims for every 100 claims filed. Greater the percentage increases the reliability of the company.

However, selecting an insurance policy solely based on claim settlement ratio (CSR) is not good. Because the CSR tends to change year on year and you can’t keep on changing your insurance companies every year. Also, a good claim settlement ratio is in no way, a guarantee that your claim will be settled. Each case is different and unique.

Incurred claim ratio : This is another ratio that explains how profitability the company runs. It is a ratio derived by dividing the total amount paid for claims with the total amount collected as premium. This number should be below 100% if the company is running profitably. However, if the percentage is way less than 100% the company may be too strict in settling claims and it may be rejecting more claims than necessary.

10) Co payment in health Insurance:

Try to select health insurance without copay. Co-pay is nothing but you agree to pay some amount of the claimed amount mostly on a percentage basis to the insurance provider, when a claim is raised. This may vary anywhere between 20-30%. A co-pay of 20% indicates that if you claim for 1 Lakh medical expenses you agree to pay 20,000 and the remaining 80,000 will be paid by the insurance provider. There are lots of health insurance providers who have no co-pay clause. Only thing is, the premium will be a little higher. But, it’s worth it.

11) Waiting periods / Exclusions in Health Insurance:

You should be very well aware of exclusions in your health insurance. Most of the policies will not cover for the following conditions:

- Change of gender treatments

- Cosmetic / Plastic surgery

- Accidents due to professional participation in hazardous / adventurous sports

- Congenital external diseases etc.,

Also, for certain Pre-existing diseases like Diabetes, High Blood Pressure, the waiting period will be for 48 months and for certain procedures like Joint replacement surgeries, Hernia, Gallbladder issues, Polycystic ovarian disease etc., waiting period of 24 months will be applicable. There may be minor modifications in the terms and conditions for different insurance providers. Read them properly.

Some policies also have waiting periods for maternity claims, however, recently more health insurance policies are available that come with maternity benefits. Also, some policies do not cover the costs of disposable items used like syringes, cotton swabs, PPE dress, surgical gowns used by Doctors, Nurses during the treatment.

12) Can Health Insurance be ported to other companies?

Health Insurance portability is possible. IRDAI has protected the rights of the insured to change the policy from one company to another company without losing the benefits. Suppose you have a waiting period of 48 months for a pre existing disease and for some reason you want to port your policy to another company after 24 months. Now, the new insurance provider has to give you the benefit of 24 months you have already gained by the old health insurance policy. Also, the new insurer has to insure at least up to the sum insured under the old policy.

But you can port it only at the time of renewal of your policy, not in between. Also, you have to write to your old insurer before 45 days requesting the shift to another company. However, the new insurer has the complete right to accept or reject your application. Also, when the insurer accepts your application, except waiting period credit, all other terms of the new policy including the premium is at the discretion of the new insurance company.

13) Points to keep in mind:

Though the health insurance covers most of the major illnesses, we should be clear that even after such scrutiny and research the health insurance we bought may not help at times. For example, cancer is covered in most of the health insurance policies. However, it says cancer of specific degree will only be covered, also for Myocardial infarction there may be a clause that says only first attack with specific severity.

So, the best thing is to be ready for the surprises. Saving and investing your money and building other income sources are the only way to move forward. Just because we have taken health insurance and Life insurance does not mean that we are financially safe.

14) Key Takeaways:

- Take health Insurance as soon as possible

- Take a family floater instead of individual policy if you are less than 35 years of age

- Don’t include your parents in your health insurance plan. Take separate plans exclusively for senior citizens

- Avoid copay

- Look for room rent sub limits, take an insurance with no capping on room rent

- Select a plan without deductibles if deductible is selected check for aggregate deductible

- Go for super top up policies and not Top Up policies

- Claim settlement ratio is not a guarantee that your claim will be settled.

- Focus, should be on creating a good corpus in long term rather than relying on health insurance policies.

{kind=link}

3 thoughts on “Health Insurance – Must Know Things Before You Buy One”