by

by We all know that having a Debt allocation in our portfolio is a must to mitigate the risk of volatility of our equity investments. It’s a general idea that debt funds can only give positive returns and can never give negative returns. However, during the Covid crisis we had seen that even debt funds can give negative returns. This has shaken many investors and has created doubts on whether to invest in debt funds or to be invested in Bank Fixed deposits itself, to avoid unnecessary risk.

“Debt Mutual Funds can give negative returns ranging on an average range from -10% to – 1% depending on the type of fund you are invested in and the global situation that exists at that time. Negative returns may exist for a time duration ranging from just three days to even a year. However, choosing a debt fund wisely is bound to give positive returns more than 95% of the time.”

In this article, we will discuss the factors that are responsible for a debt fund to give negative returns and how we can handle it.

- Why may returns be negative?

- Negative return due to Interest risk

- Negative returns due to Credit risk

- Negative returns due to liquidity risk

- Negative return based on time of investment

- Negative returns comparison for different funds

- How long the negative returns may be?

- How can it be managed?

Why Debt Fund’s returns may be negative?

There are four major factors that affect the debt fund returns:

- Interest Risk based

- Credit risk based

- Liquidity risk based

- Time of investment

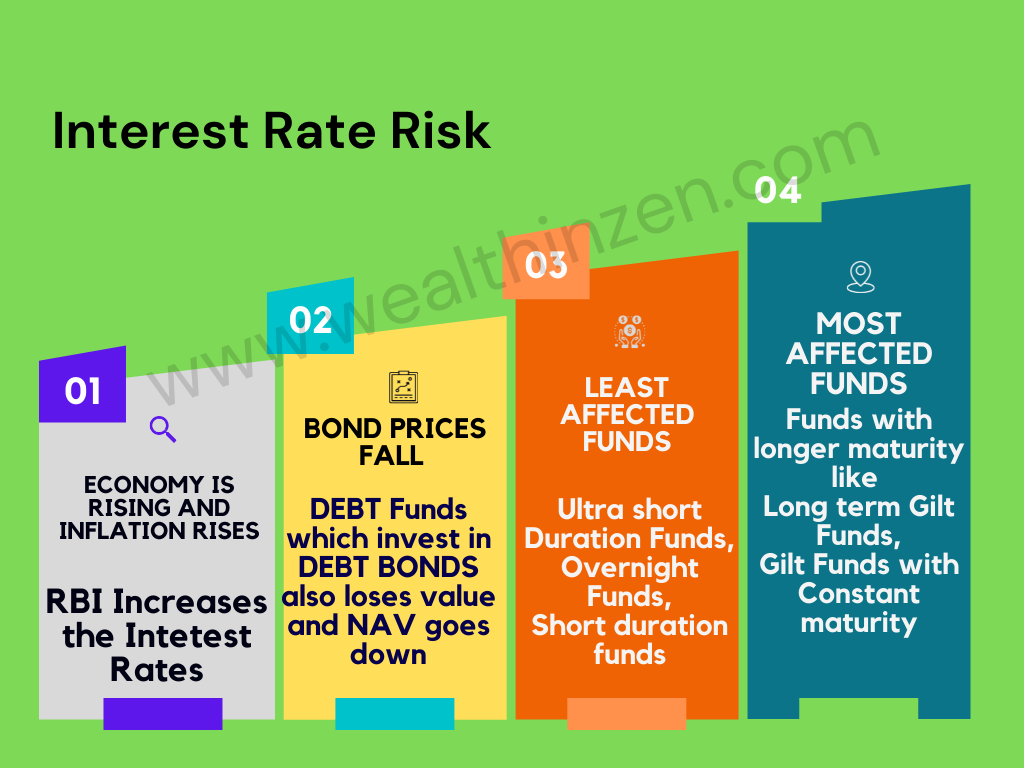

Negative return due to Interest risk:

The most common risk of debt mutual funds is the interest risk involved in it. Interest rates typically rise when the economy is growing and decreases when there is downfall. Interest rates and the bond price has an inverse relation. That is if the interest rate decreases the price (NAV) of the debt mutual fund increases and thereby returns increase. Also if the interest rate increases then the NAV decreases and thereby returns decreases leading to even negative returns at times.

Suppose, if you are investing a lump sum amount in a debt mutual fund and the next day the RBI increases the interest rates it is going to affect the prices (NAV) of your fund and may have a negative impact.

Also, interest risk depends on the type of fund you invest in. For example if you are investing in a long term gilt fund with longer maturity say for ten years or more, higher will be the impact while a Ultra short term Debt fund with maturity of less than 90 days may have lesser impact.

Negative return due to credit risk:

Debt mutual funds invest in debt bonds. Bonds are nothing but an agreement between the lender and borrower. The borrower (Bond Issuing company) gets money from the lender (retail investors who invest money in debt funds) and in return they give the investors an interest from the profit they assume to make in the future. It is important to note that this is not a guarantee. If the company that issued the bond is not able to repay the loan due to loss or bankruptcy then it is considered to be a defaulter.

This risk of default on a debt security is called credit risk and will impact the portfolio returns. If the fund manager has invested a huge part of money in that default security, then it will hamper the fund to the extent of its weight in the portfolio.

To avoid this kind of defaults and to help the investors to take an informed decision the bonds are assigned Credit Ratings by agencies like CRISIL, CARE and ICRA. These ratings are given on the basis of the ability of the bond issuer to repay the loan without defaults.

AAA rating for a corporate bond is said to be the highest quality with negligible risk of default on payment of interest and repayment.

It is to be noted that if you find a debt fund offering a very high rate of interest in a shorter duration time it may be because they are investing your money in poor rated bonds which promise to give higher returns. Below is the CRISIL Rating scale for the bonds in which the Debt mutual Funds invest.

| CRISIL Rating | Safety Level |

| AAA | Highest Safety |

| AA | High Safety |

| A | Adequate safety |

| BBB | Moderate safety |

| BB | Moderate Risk |

| B | High Risk |

| C | Very High Risk |

| D | Default or expected to be default soon |

These Ratings can be seen easily in websites like Value research, Money control, Morning Star sites. Choosing a debt mutual fund investing in poor rated bonds may seem to give high returns for the time being but the risk of default is very high.

Negative returns due to liquidity risk:

Investopedia defines Liquidity as the ease with which the asset can be converted into ready cash without affecting the market value. In other words it defines the ability of the fund to distribute money to the investor in case of redemption without any difficulty.

Though the debt funds are highly liquid and there is nothing to worry about redemption, some black swan events may cause unexpected issues in liquidity. For example, during Covid times the economy went bad and the equity market hit the rock bottom. Shocked retail investors started redeeming all the money from both equity and debt funds.

When there is increased demand for redemption in a very short period of time the bond prices fall greatly and it impacts the portfolio returns. People who started their investments just before the covid outbreak were in a shock to see even their debt investments in red with negative returns.

Another example of liquidity risk is the one that is linked with credit risk. Best recent example for this, is the closure of six debt funds of Franklin Templeton on April 23,2020. All were debt funds and people were investing in these funds overwhelmingly as the returns were very good.

However, when the pandemic hit and the people marched for redemption Franklin Templeton could not meet the redemption requests.

This is because they had invested in companies which are low rated and highly illiquid. As a result, they could not meet up the redemption requests as cash was not available with them to give to the investors. Finally, SEBI has to intervene and fined Franklin Templeton a penalty of 5 Crore and return 450 crores collected as investment management and advisory fees in the last 22 months and imposed ban on launching new debt schemes for a year.

Investors had to wait a year to get their invested amount due to their closure. However, the closure of those debt funds is seen as the best possible move for the investors. If the fund has not closed then, to meet the investors redemption request it would have been forced to sell the good quality assets and that too at a deep discount thereby making severe loss to the investors.

Negative return based on time of investment:

So as discussed above, any of the reasons may give a negative return in your portfolio.

It also depends on the time you invest. For example you are investing a lump sum today but there is an announcement from RBI the next day regarding change in interest rates, then it will impact your portfolio, as it will be too early for the fund manager to manage the risk.

Below is the weekly chart of SBI Magnum Constant maturity Fund (Direct Growth). You can see that depending on the time period you invest (orange arrow) even debt funds may give negative returns. (Source – TRADE POINT)

Rolling return comparison of different debt mutual funds:

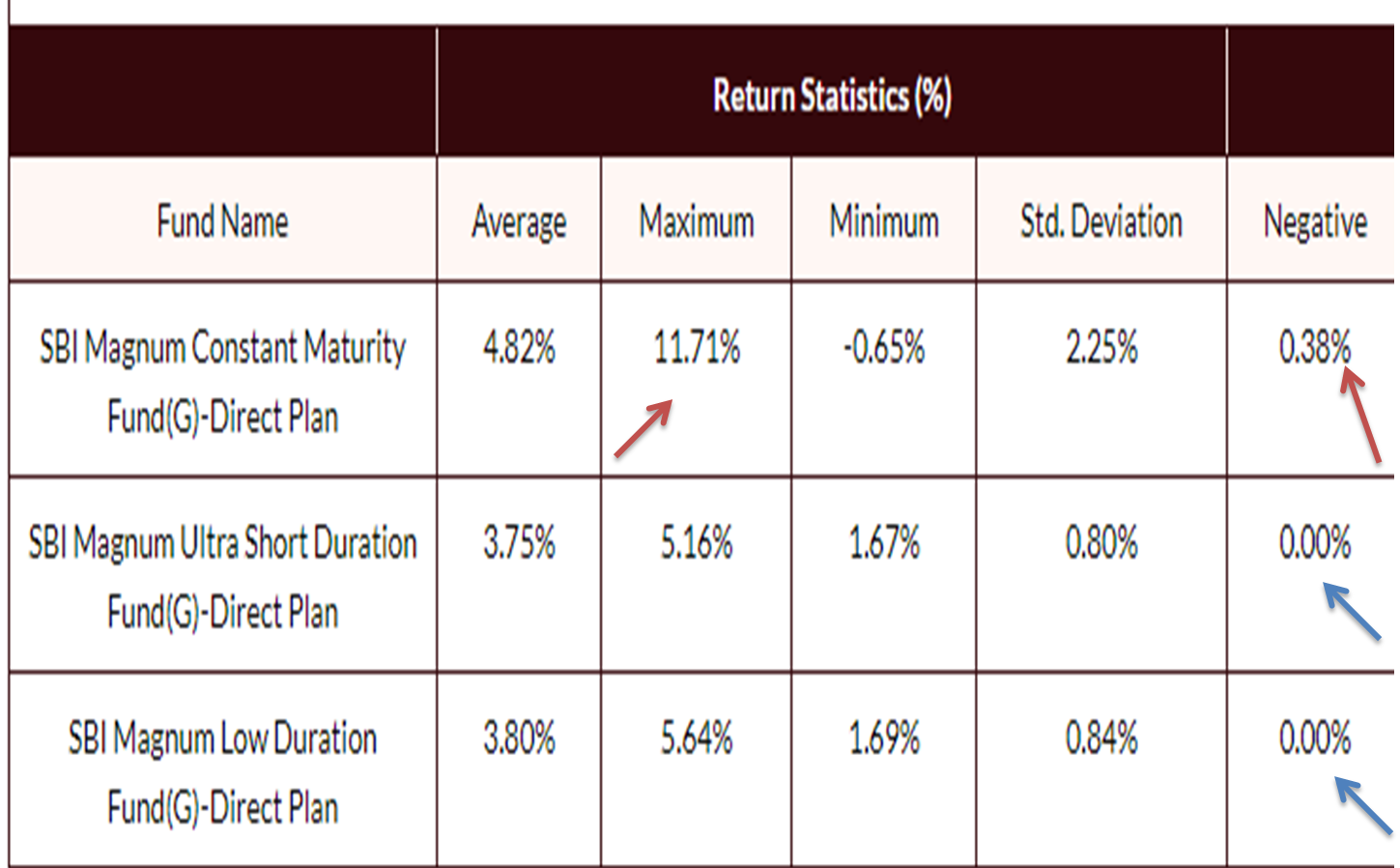

For an understanding of how funds with longer maturity have more interest rate risk and how it affects the portfolio, we can compare and see three different fund types belonging to the same Fund House company from 2005 – 2022 (source – prime investor.in) with roll over for every six months. The funds compared are :

- SBI Magnum Constant Maturity fund (G) Direct plan – Long duration Gilt fund with maturity period of 10 years – Orange line in Graph

- SBI Magnum Low duration Fund (G) Direct – Maturity period six months – 1 year – Purple line in graph

- SBI Magnum Ultras Short Duration Fund (G) Direct – Maturity period three – six months – Red line in graph

We can see that in the above graph the SBI Magnum Constant Maturity fund (G) Direct plan, Long duration fund has given the maximum return of 11.65% and at the same time lowest negative return of -0.65% also. This indicates that the volatility is very high in that fund. But has the ability to generate high returns also. If you are investing for a long term you can consider buying this.

The table below shows the return statistics of these three funds from 2005 – 2022 with roll over for every six months. The red arrow indicates that SBI magnum Constant maturity fund with Longer maturity has given a negative return for a period of 0.38% from 2005-2022 while the negative returns were zero in low duration and ultra short duration funds (blue arrow)

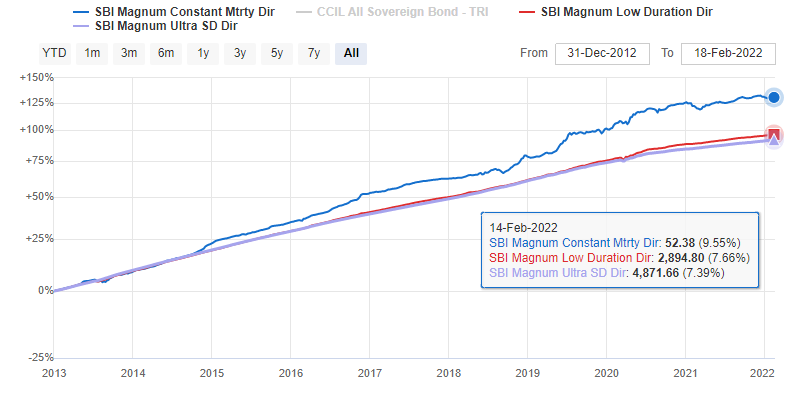

You can think that since the Constant maturity fund has given negative returns 0.38% of time in its 17 year duration, it is risky to invest in it. But wait, take a look at the returns of these funds for the past 10 years from 2012 -2022 in the image below. Source (Valueresearch.com)

| Fund Name | Investing Duration (2012 -2022) | CAGR | Average Maturity Time |

| SBI Magnum constant maturity fund | 10 Yrs | 9.55% | 10 Yrs |

| SBI Magnum Low duration fund | 10 Yrs | 7.66% | 6 – 12 months |

| SBI Magnum Ultra short duration fund | 10 Yrs | 7.39% | 3 – 6 months |

As the maturity period increases the return also increases. In the table above you can see the CAGR of SBI Magnum constant maturity fund with average maturity period of 10 years is the highest. So, it all comes to how long you want to get invested. If your investment horizon is less than three years then it is better to invest in short duration funds rather than longer duration funds. This is because you can avoid the volatility associated with these funds.

Below image from valuresearch.com shows the performance comparison of these three funds in short term 1 year (from Feb 2021 – Feb 2022). You can see how the Long duration fund (SBI magnum constant maturity) Blue line in the image gives poor returns as on Feb 5 2022 compared to other two shorter duration funds. So if your investment horizon is shorter longer maturity bonds are not to be considered.

How long the negative returns may be?

Hope that you are clear that even debt funds can give negative returns at times and now the next question comes – for how long will this negative return be?

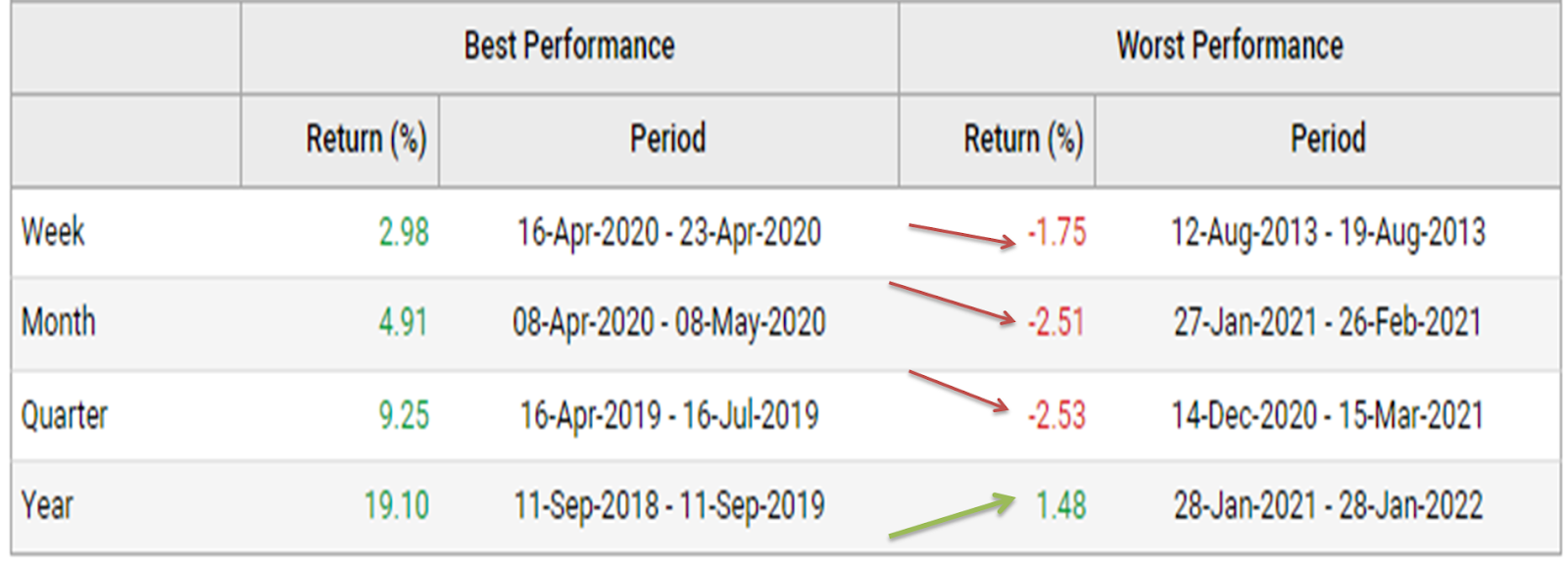

Though the funds based on various reasons like interest risk, credit risk and liquidity risk can give negative returns, it is short lived usually. Since we had seen in the above example that SBI Magnum constant maturity fund has given negative returns at some point of times, we will see how long it existed in the following image (valueresearch.com):

Red arrows indicate the worst performance of the fund in the period mentioned on the right side. The data is for ten years from 2012- 2022 and you can see that if you have stayed invested at least a year in this fund the worst case scenario is a return of positive 1.48 %. In a period of ten years the worst performance of the fund in any given year is 1.48% positive return.

Thus even though negative returns in debt funds are a possibility, in the long run it is more likely to give you positive returns only. Also the period of negative returns as you can see in the above table is very short lived.

How to manage this?

- One thing you can do is instead of investing as lump sum, bring your money to debt funds slowly in the form of SIP. Even SIP may have some disadvantages. You can read it here.

- Invest in funds that have lower credit risk and funds that invest in AAA Rated bonds. One way to avoid credit risk is to invest in debt mutual funds that invest only in government bonds and government securities.

- If you are investing for more than ten years SIP in long term funds like Debt Gilt funds (Like SBI Magnum Constant maturity fund) is a good option to consider. Because these funds have almost negligible credit risk as they are backed by the Government. But remember that they have interest rate risk due to longer maturity. So, to benefit from this fund you have to invest for a longer period of time.

- If your investment horizon is shorter say for one – three years then invest only in short duration bonds which invest in either govt securities or good AAA rated corporate bonds.

- Never, invest in a fund just because it shows high returns in the past year or so. It may have invested in poor rated companies. If you are investing in low quality debt funds you are bound to burn your fingers.

- If your investment horizon is less than three months consider investing in either overnight funds (invests in government securities) or Liquid ETFs (Know more about Liquid Bees / Liquid ETFs here)

- All the opinions discussed above are my personal views and there may be some bias. So, consult with your financial advisor before investing in any fund and be sure whether it is suitable for you.

One thought on “Can Debt Mutual Funds give negative returns? Why and What you can do about it?”