by

by When it comes to diversifying your money across assets, Debt is an unavoidable and very important component. Anybody who invests 100% in equity is bound to see some bouncers in his/her personal finance life. However, when most of us will invest in fixed income schemes, the options we choose are usually Bank Fixed deposits, Post office schemes, Recurring deposits, chits.

Debt mutual funds are a less explored thing in India. Even a person who has his investments in equity mutual funds may not have invested in debt mutual funds. Through this article I am going to tell five top reasons to invest in Debt Mutual funds. At the end of this article, you will understand why a debt mutual fund should be a must have allocation in your portfolio.

Top Five reasons:

- Change in trend

- Diversification and Flexibility

- Liquidity

- Tax benefits

- Rebalancing your Portfolio

1.Change in trend:

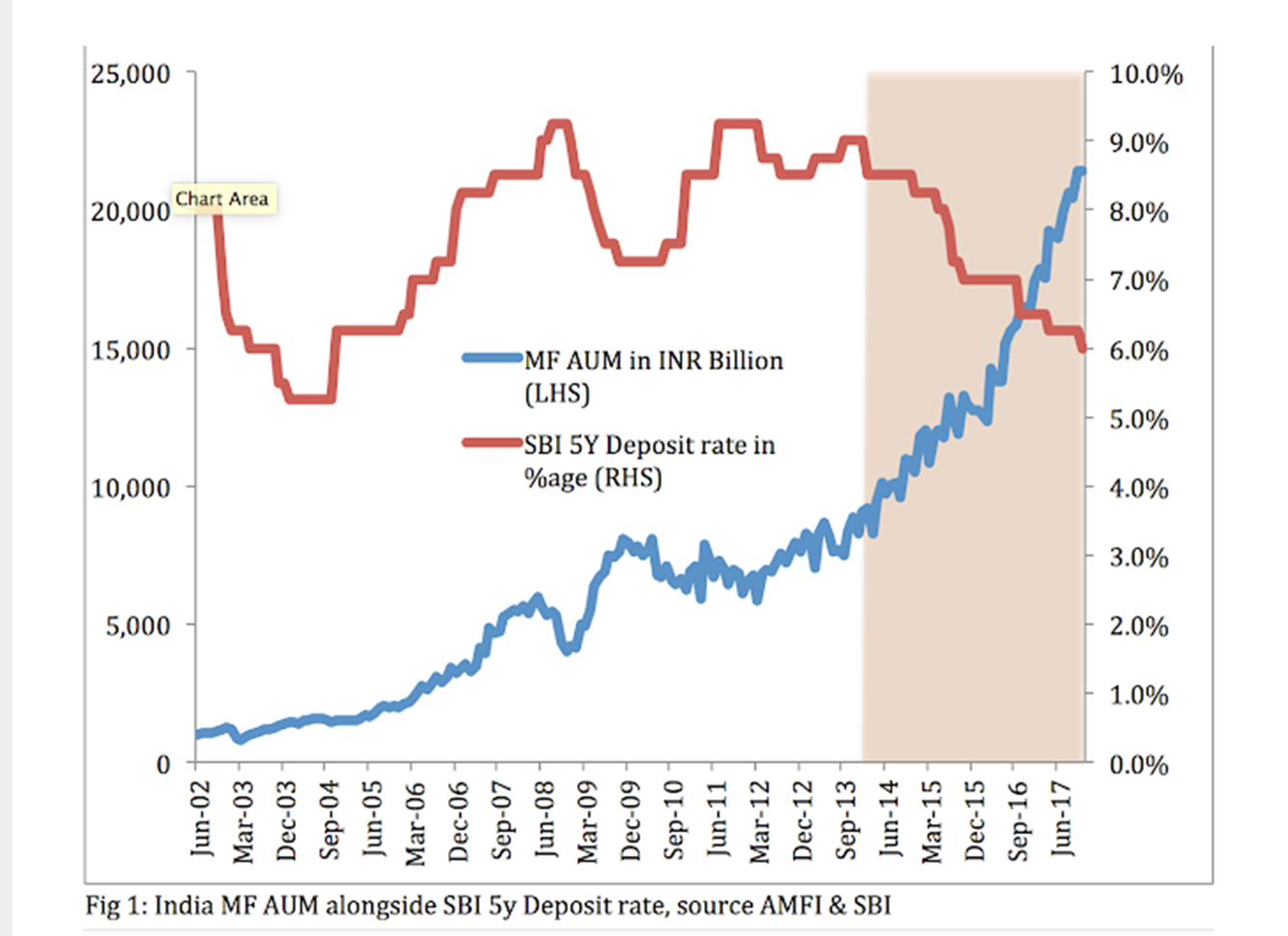

As the interest rates are getting smaller with each passing year, the sentiment of investors has changed greatly in recent times. Even PPF interest rates declined a lot and are now at 7.1% per year which is just breaking even with the average inflation rate. If we consider investing in a Bank Fixed deposit, then we are more likely deteriorating our wealth. Inflow of money into the mutual funds in recent times has greatly increased when compared to the Bank Fixed deposits. You can see in the image below:

This image clearly shows how the investor’s sentiments are changing rapidly and more people look into investing their hard earned money in mutual funds than Bank Fixed Deposits. Debt mutual funds are different from equity mutual funds and the awareness for the former is very little compared to the later. Debt mutual funds (depending on the fund you choose) in the long run can give a return that can beat inflation or at least give return greater than the Bank FD.

With the changing trends, it is always wise to step out a little and see why Debt mutual funds can be a good alternative for you.

2. Diversification and Flexibility:

Debt mutual funds offer diversification of your portfolio and it is safer than Debt bonds. (Debt mutual fund and Debt bonds are two different things and don’t get confused)

In debt bonds your investment amount is exposed to a greater credit risk in case of default of the bond issuer. However, in debt mutual funds, the fund manager invests in various bonds including government securities making them less prone to credit risk.

Also, anybody can start investing in a Debt mutual fund even with a small amount of 1000 INR. You can invest either as a lump sum amount or in SIP mode. Most of the debt mutual funds are open ended funds which allows you to exit the fund whenever you want.

3. Liquidity:

Liquidity refers to the ease with which the asset you have invested can easily be converted to cash. In other words, it simply means the time to get the money in your hands, so that you can use it for your purpose. Bank Fixed deposits may not be that liquid as it requires some time for the bank to close the deposit, to process and to hand over the money to you. Debt mutual funds, unlike Bank FDs, are open ended funds. There is no lock in period. There are multiple options available in case of debt mutual funds, based on when you want to redeem the money.

If you want to park your excess money for a few days to one / two years and get a return which is equal to your savings account you can invest in Liquid funds, short duration funds, ultra short duration funds. If you are planning to invest for a longer period of time say for 5-10 years you have gilt funds and other longer duration funds.

4. Tax Benefits:

The most important benefit of investing in Debt Mutual Funds is the tax benefit you get. Taxation of Debt Mutual Funds is based on the investment period. Any investment less than three years is considered for Short term Capital gains and investment for more than three years will come under Long term capital gains. Since, the short term capital gains are taxed as per the income tax slab of the investor, it does not make a difference whether you invest in Bank FD or RD. And is not of much help in the taxation part.

However, the real benefit comes when you invest in Debt funds for a very longer duration of time like 15 years – 20 years. This is particularly useful for those individuals, who come under 20% or 30% tax slabs. Even though the long term capital gains are taxed at 20%, you are allowed for indexation benefit.

Indexation allows you to reduce the purchase price of the investment by considering the inflation effect on the investment. So, you can adjust your capital gains to lower your taxes while this is not possible in Bank FDs. Investments with a very long horizon like 10-15 years can be very tax effective and can bring down the tax to be paid from 20% to just 15-16%.

If you come under the 30% tax slab then you are going to reduce your taxes on capital gains to a great extent as you are liable to pay only 20% (after indexation may be 16%) capital gains tax. If you had invested the same amount in Bank FD you would have paid 30% on capital gains.

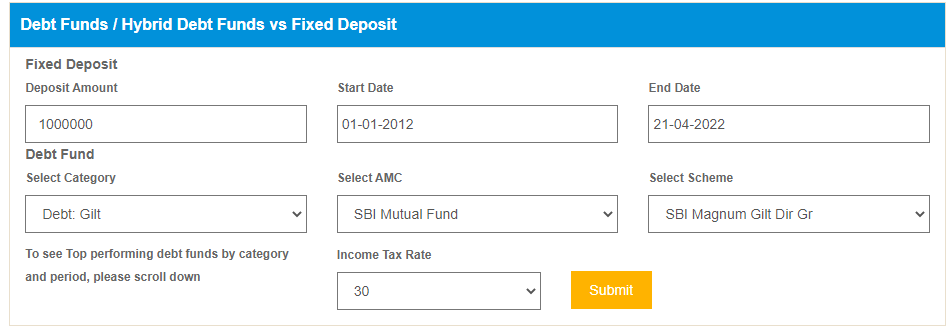

If you are still not convinced of how beneficial this is in the long run, let us see the following example, how the returns vary when you invest in Debt Mutual Fund Vs Bank FD.

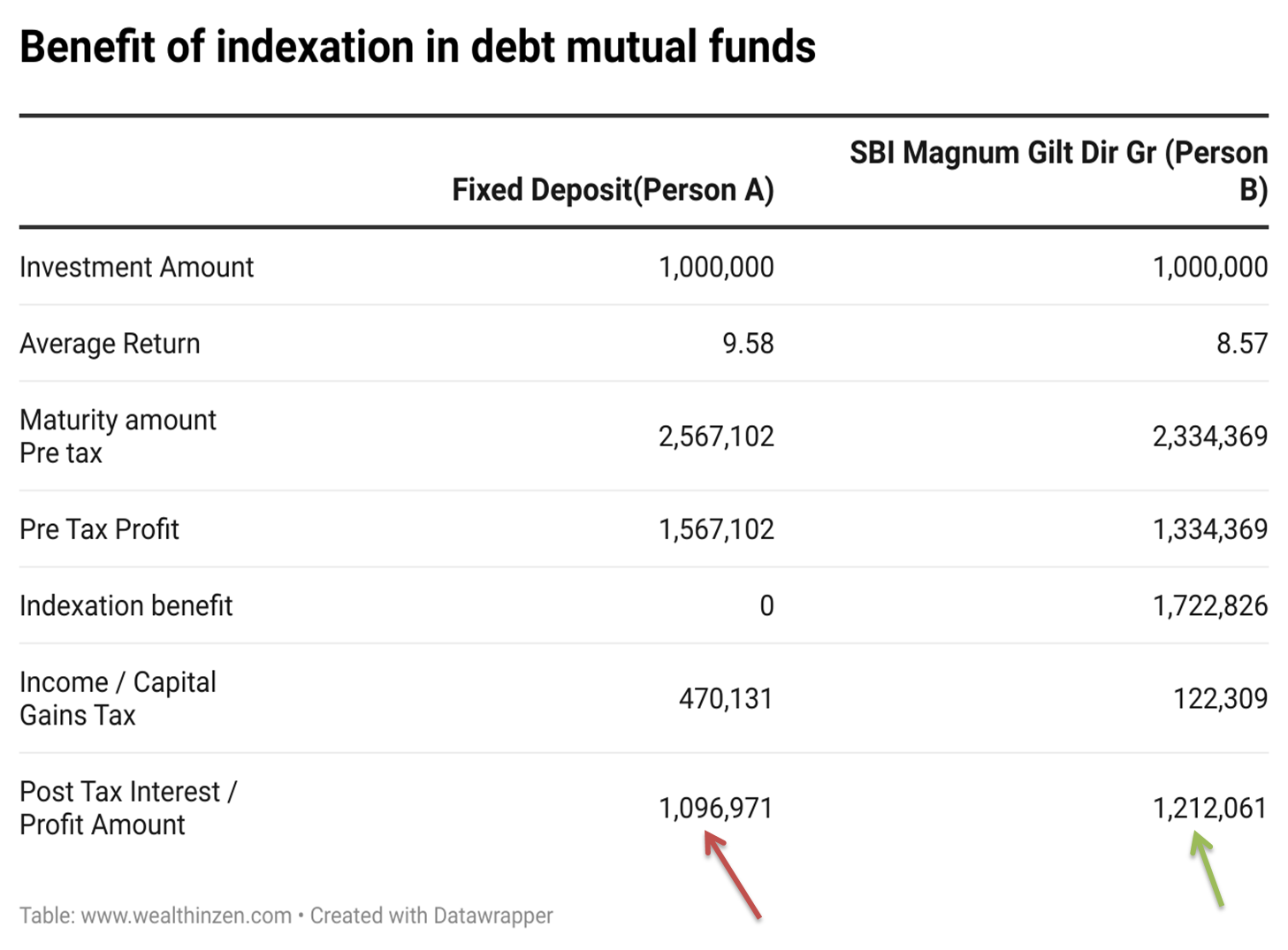

Let us assume that Person A invests 10 Lakhs in BANK FD on Jan -01-2012 with average interest rate of 9.58% (The Fixed deposit interest rate is based on historical State Bank of India Fixed deposit rates for different deposit terms) and Person B invests 10 Lakhs in SBI Magnum Gilt fund (Direct Growth) on the same day, with a CAGR of 8.57% till date (22-April – 2022)

Both invest for a period of ten years from 2012 – 2022 and both come under the tax slab of 30%. The returns they get pre and post tax are shown in the table below.

You can see that even though the pre tax profit of SBI Bank FD is greater than the Debt mutual fund returns, the post tax return / profit is higher for Debt Funds (green arrow) when compared to FD Returns (red arrow).

So, we can see how the indexation benefit has helped us to reduce the tax burden. Point to be noted is in this example, the SBI Fixed deposit returns are shown to be around 9.58% . This is the average of FD interest rates from 2012. But, we know that the interest rate of FD in SBI is around 5.5%-6% today. These interest rates are bound to fall in coming times, most probably. That is what history tells us.

Imagine with such a poor interest rate and with no taxation benefits we are bound to impede our growth of money. This makes Debt funds a must have thing in your portfolio.

5. Rebalancing Portfolio:

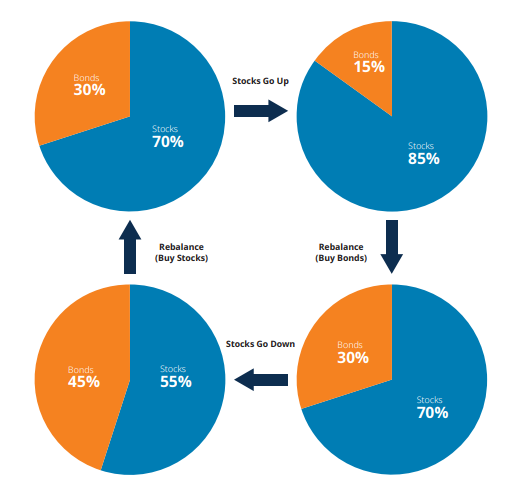

While Portfolio allocation can be done easily at the start of your investing journey maintaining the same allocation till the end of your goal requires some effort. For example when you start your investing journey you may allocate 30% to Debt funds and 70% to Equity or stocks. However, the equity markets are more volatile and sometimes they run up too much. With the profits more in equity now, your portfolio may now have 85% of equity allocation (with the profits) and debt funds may have 15% allocation.

Now, we can sell some equity and book the profit and re-invest that amount in debt related bonds / funds, so that the allocation comes back to 70% equity allocation and 30% Debt allocation. On the contrary, if the stock market gives poor returns, making your allocation 55% in equity and 45% in debt, then sell some debt and increase the equity exposure to 70% and maintain the debt allocation to 30%. This will help you to buy the stocks at lower prices and also help you to maintain a balanced portfolio.

Source : https://www.miraeassetmf.co.in/knowledge-center/how-does-portfolio-rebalancing-happen

Rebalancing portfolios has been proved to be effective in not only increasing the returns but also in reducing risks in case of market crash or some black swan moments.

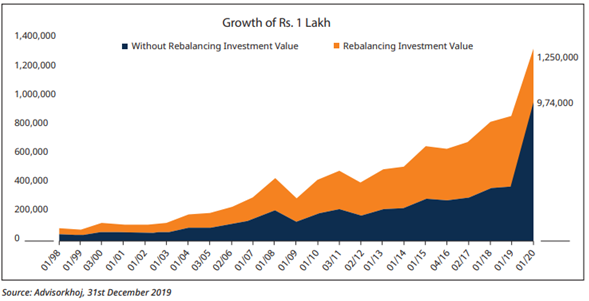

Let us see an example (Picture below). We will use Nifty 50 as the proxy for equity and Nifty 10 year G-Sec Index as the proxy for debt. Let us see how your investment would have grown over the last 20 years without any rebalancing.

Your investment’s market value at the end of 2019 would have been around 9.7 lakhs. However if you would have done annual rebalancing the value would have grown to 12.5 lakhs, an incremental gain of 2.7 lakhs.

To do this kind of rebalancing at will, your money should not be locked in like PPF or any FD which cannot be assessed when needed. In these kinds of situations debt mutual funds allow us the liberty to withdraw funds at a shorter duration and invest in equities and rebalance our portfolio if the need arises.

Key Takeaways:

- Debt Mutual funds are an alternative investment option for conventional Bank FD / RD

- Though in the short term the advantages of a debt mutual fund may seem to be insignificant, in the long run it is definitely advantageous.

- Selection of debt funds depending on your investment horizon is very important as it will directly impact the returns.

- If you are in a 20-30% tax slab and you are investing in fixed income instruments for your retirement / long duration portfolios then debt mutual funds should definitely be explored.

- Rebalancing your portfolio from debt to equity in regular intervals (at least once in a year) will minimize risk and maximize returns.

- If you cannot find a good debt mutual fund on your own, you can ask a fee-only financial advisor to decide a better fund for you, based on your expectations and requirements.

One thought on “Debt Mutual funds: Top 5 Reasons to have it in Your Portfolio (Last Two are Very Important)”