by

by We all want the best in everything we choose. Life insurance is not an exception for that. People tend to keep on looking for the best life insurance plans and the search for that never ends. Choosing a Life insurance should be easy and should not take you more than a day or two to select one. However, the life insurance companies come with different products / plans each day and make the decision making process a highly confusing one. One such plan is the “ Life Insurance with Guaranteed returns and Return benefits on maturity .“

Are these plans really worth buying and the returns they give are really worth as advertised and marketed? Well, let us find this out in this article.

How does it work?

Life insurance with returns mostly come under these two categories:

- Life insurance with return of the premium on maturity

- Life insurance with guaranteed returns

The first one is similar to that of term insurance where you take insurance for a particular period say for 20-30 years and pay the premiums every year. At the end of maturity period if the insured person is alive, he/ she will get the entire premium amount paid. This is claimed to be a good option since it gives you the entire premium amount you pay during the insured period. Seems good right? Wait, I will discuss this in the later part of this article.

The second one is a little different from term insurance. In this, you will pay a fixed amount as premium every month for a specific period, say 6-10 years. After that, you will be paid out a guaranteed money every month which will be greater than the amount you paid at the start of the policy.

There are many variations in these plans like different payouts and different time periods. However all the plans will be more or less like this only.

Life Insurance with return of the Premium on maturity:

Most people think that life insurance is a waste of money. This is because they don’t see any benefit for the premiums they paid during the entire term. Lot of people even avoid taking life insurance just because of this. Insurance companies are way smarter than the public and they launched a plan which guarantees them that the entire premium they paid will be given back at the end of maturity period, if the insured person is alive.

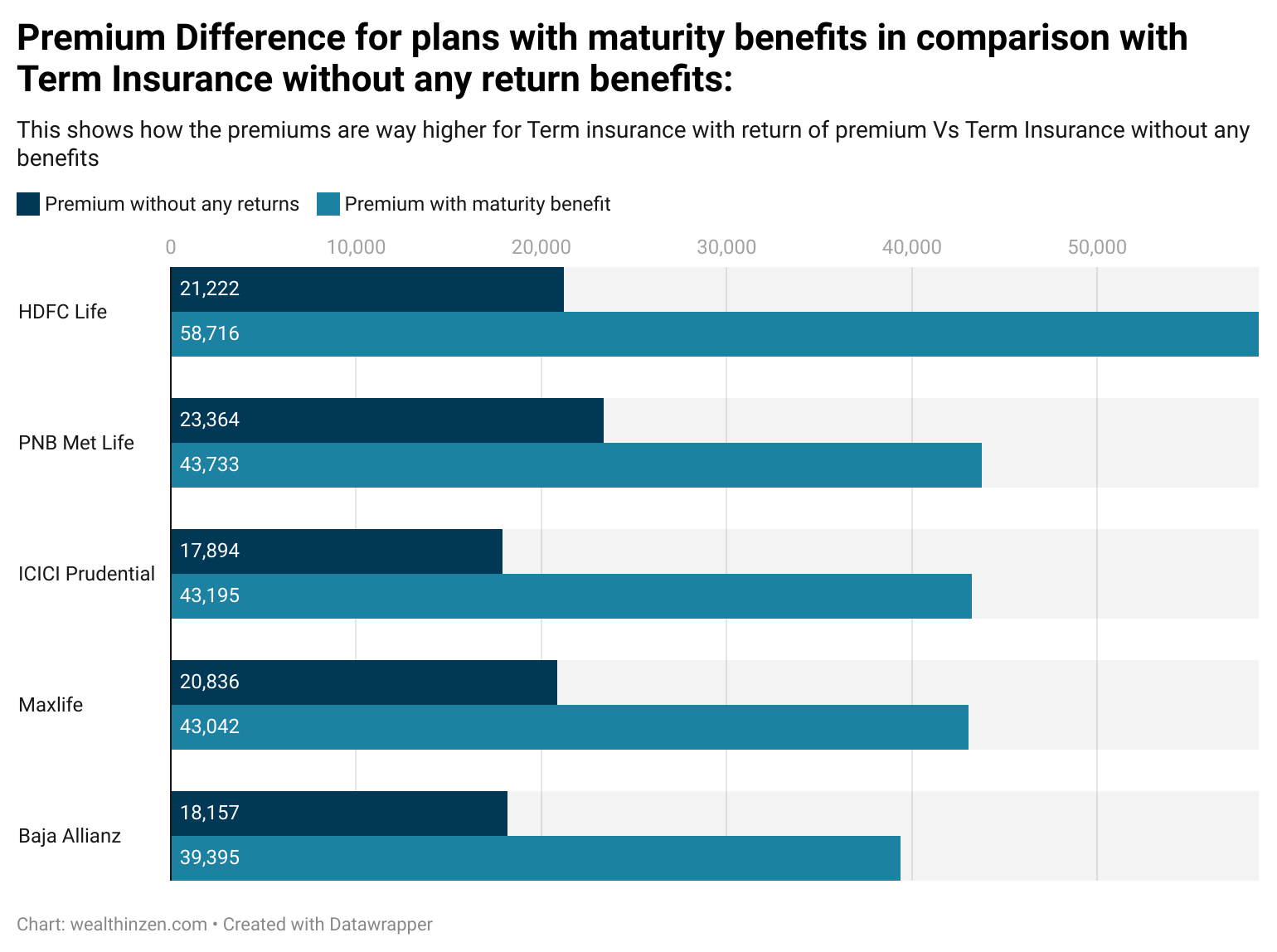

If a person has paid premium of 20,000 INR for a term of 30 years, then at the end of 30th year, if the insured person is still alive then he / she will receive the entire premium amount of 6,00,000 Lakhs (20,000 * 30 years). So, you will get 6 Lakhs at the end. Sounds fantastic right? However, for this plan the premiums are way higher than a pure life insurance without any maturity benefits. You, can see this in the image below which shows how the premiums differ between a Life Insurance with return / maturity benefits and a plain Life Insurance, for the same coverage of 1.5 Crores:

As you can see, in plans with maturity benefits, you are paying a very high premium, in some cases 150-170% more than a normal term insurance without any benefits. I can hear you, so what? I am getting these amounts at the end of my term insurance period right?

But wait, for illustrative purposes let us assume that you buy a plain HDFC Term insurance for a period of 25 years with coverage of 1.5 crores by paying a premium of 21,222 INR Per year. Instead of going for an insurance plan with return benefits which requires a premium of 58,716 INR per year for the same amount of coverage (1.5 Cr), you are buying a plain one.

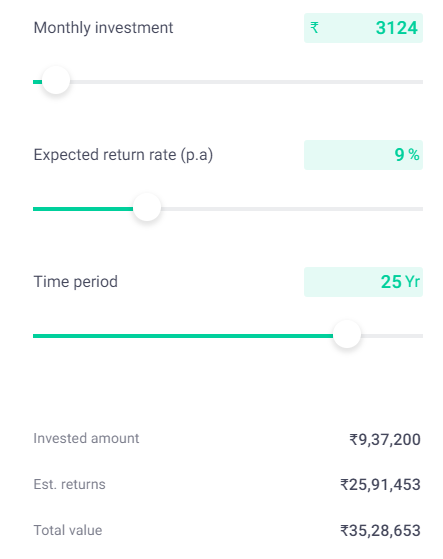

So, per year you save (58,716 – 21,222) = 37,494 INR

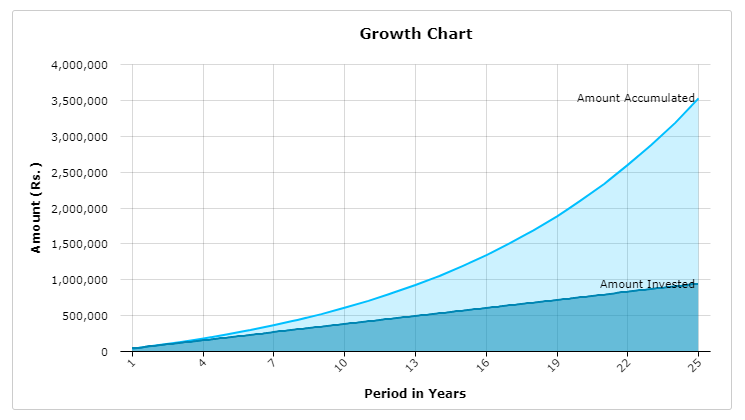

If this is divided by 12 (12 months in a year) and you start investing that money (37,494 / 12)= 3124 INR every month in a mutual fund SIP. Even if you get a nominal return of 9% CAGR you will end up with 35,28,353 (Thirty Five Lakhs) at the end of 25 years.

You can see how your money would have grown in a 25 year period. However, if you have selected a plan with maturity benefit you would have end up with just (58,716 * 25) = 14,67,900 INR at the end of 25 years.

14 Lakhs To 35 Lakhs. Whooping difference right? I purposely put the returns of a mutual fund to be 9% only to not exaggerate the returns. Even with these nominal returns the difference is mighty, which is around 140% more returns. Still thinking about getting life insurance with the return of the premium option??

Life insurance with guaranteed returns:

These are monthly income schemes provided by the insurance companies, in which the insured pays a premium every month for a particular period chosen by the insured person. The premium varies depending on the amount insured and the duration of the policy. After paying the premium for the particular period, comes the period where the insurance company will pay the insured every month a fixed amount. This amount is usually claimed to be higher than the amount paid by the insured.

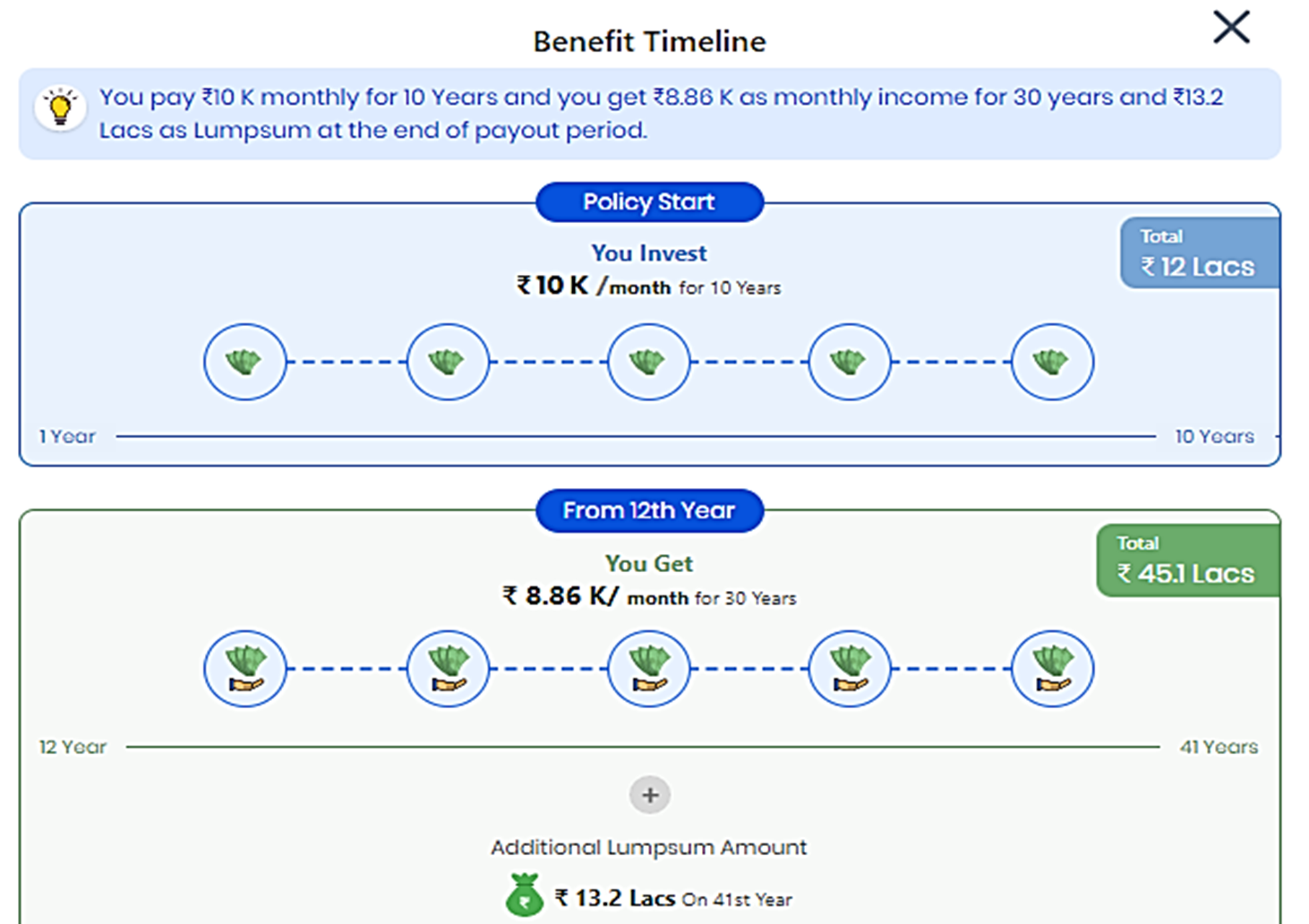

An example image (Source- Policy bazaar) is shown below:

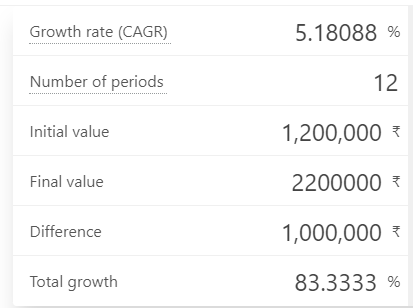

In the above example, you pay / invest 10,000 INR every month for the first 10 years and in return, from the 13th year you will get 18,400 INR every month as a guaranteed return. So, your investment is 12 Lakhs for the first ten years and the return you get after 22 years is 22 Lakhs.

So, you invest 12 Lakhs and then you get 22 Lakhs. That is 83% absolute return on your investment. But you get that amount in a span of 12 years after your first ten year premium payments of worth 12 Lakhs.

That would roughly come to a CAGR of about 5.1% as shown in the image below even though the absolute return is 83%. This means that your 12 Lakhs investment grew to a meager 5.1% per year which is less than a Bank’s Fixed deposit. If an inflation of 6% per year is considered you have a negative return in reality.

Another important problem with plans like this is that they give very very very poor coverage. The above said plan gives cover of just 12 Lakhs in case of any untoward events. If your annual expenses are 4 Lakhs per year your family cannot even manage for four years with this money. Why should you waste your money by selecting such a plan? Well, not anymore, at least in my opinion.

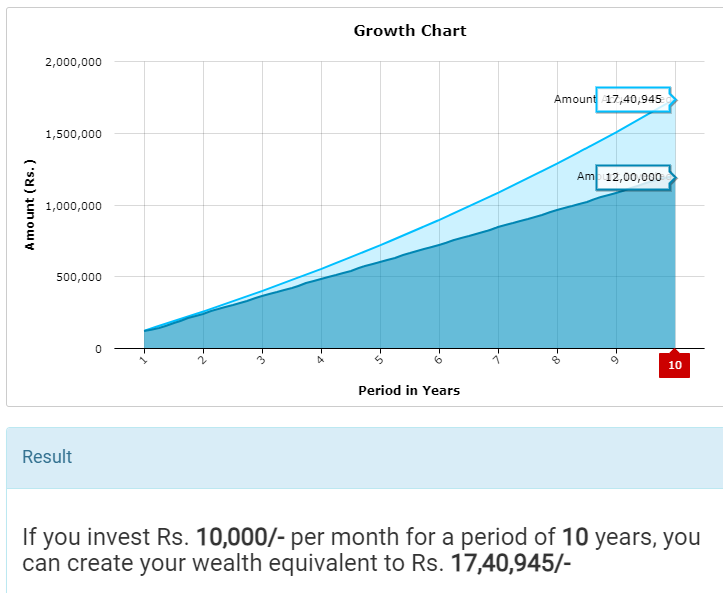

Again let us consider a situation where you will invest differently. Let us assume that instead of buying this plan, you start investing 10,000 every month in a passive index mutual fund in SIP mode for the first ten years. Now even if the returns are just 7% per year (calculated as XIRR) your investment will grow to 17,40,945 INR.

I can hear you say that,” Hey in the policy plan I get 22 Lakhs but here I am getting only 17 Lakhs right?” Yes but you are not getting 22 Lakhs in the eleventh year right? Your payout starts only by 13th year (See image). Two years your investment sits idle without any benefit and you start getting the payout in small amounts on a monthly basis from thirteenth year. Time is money and sooner you get the money in your hand higher the value. That’s why they payout your money in a very slow manner with very poor return which is difficult for a common investor to understand.

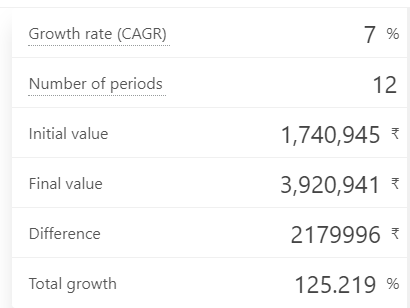

Coming back to our calculation, let us assume that after 10 years of investing in SIP mode in an index mutual fund,you leave that 17 Lakhs amount to grow for the next 12 years. You don’t withdraw any amount and you don’t invest any further also. Let’s see how this would have grown.

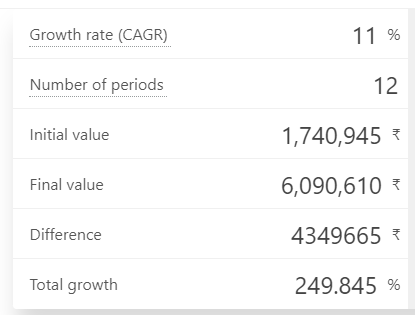

As you can see you would have ended up with a final value of 39 Lakhs instead of just 22 Lakhs at the end of 22 years. I had just taken a growth rate of 7% which is very very low when compared to the past historic returns of index funds. (Average index return is 11-12%). Let us see what will be the final value you will get if the returns are 11% per year:

You get 60 Lakhs at the end of 22 years instead of just 22 Lakhs as promised by the company. So these insurance companies mislead you by using terms like “ Get 2X returns, 3X Returns” and make you believe that you are getting high returns. But, in reality these plans hamper your future returns to a great extent and these insurance companies use your money for their growth and give you peanuts.

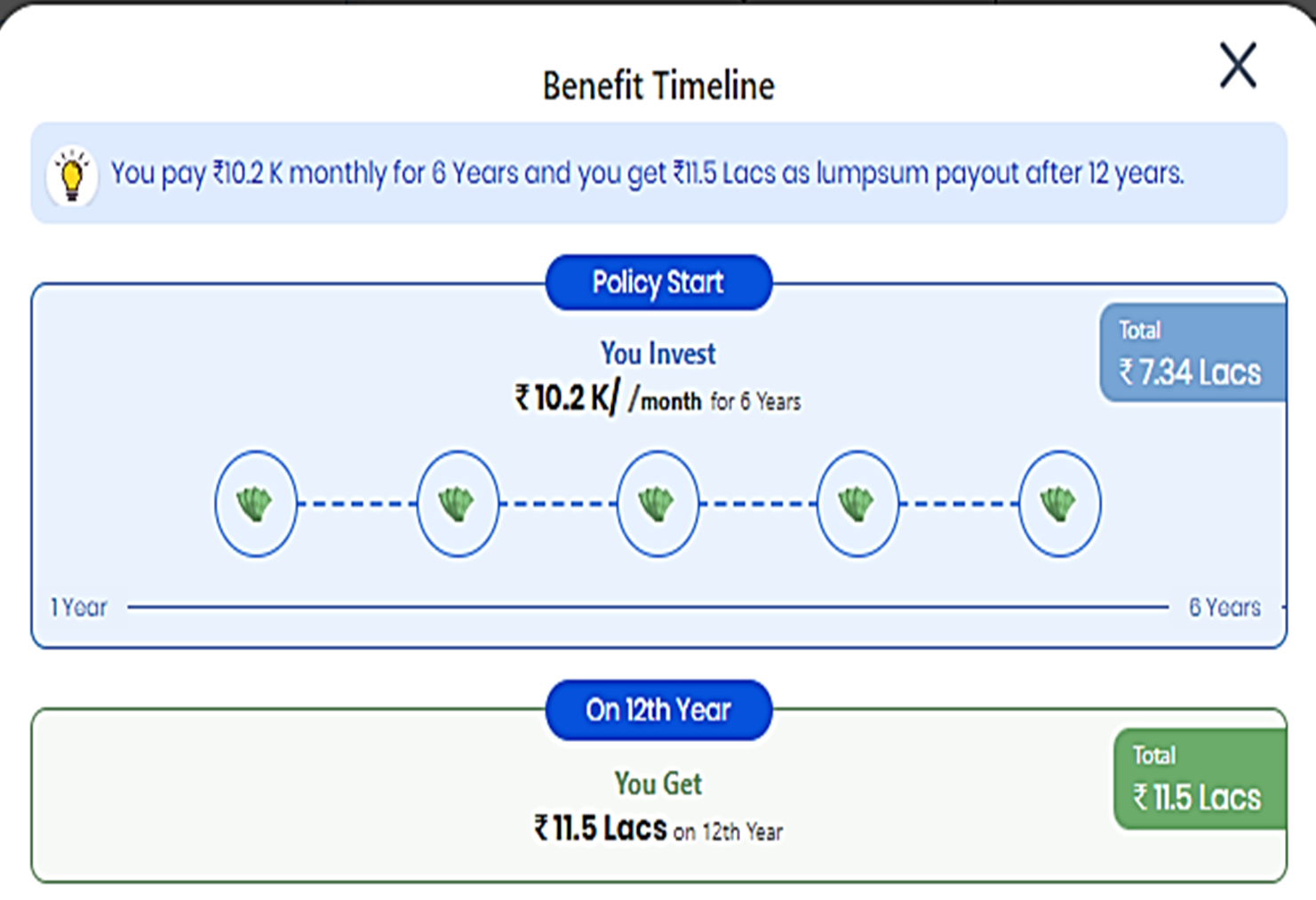

There are few other plans available as shown in the following images:

In the above plan don’t think that they are giving you higher returns by seeing 45 Lakhs. They pay in thirty years unlike the plan we discussed previously where they pay in ten years. Remember, time is money.

As you can see, all these plans are more or less the same. They get as much possible money from you initially and pay you later with very poor returns / interest.

So, what to do?

Let’s blame these corporate companies for our lack of knowledge? Companies will always try to deceive us. However, nothing is hidden. They had put up everything in their documents. We can’t expect them to be transparent because they run their businesses like that. That’s their money making strategy. It’s our duty to analyze a plan / policy before investing. In India most of us invest in these plans because we lack financial literacy and most of the insurance plans we take are influenced by our friends / relatives.

Also, we don’t think in a longer time frame. To see the results as stated above, you have to wait 20-30 years. The problem is do you have the patience to believe in your strategy and sit silently through those years? Do you have the guts to say to your friends / relatives who are insurance agents and pressurize you to invest in these types of plans? If you already have one such insurance plan do you have the courage to discard that insurance scheme and buy a simple term insurance? The answer lies with you. Find it before it becomes too late. If your mind is not free and clear you cannot become financially free / Independent.