by

by PPF or Public provident fund is a government backed Tax saving instrument with a guaranteed return, with a lock in period of 15 years and ELSS or Equity Linked Savings Scheme is a mutual fund investment option where the returns are market linked with a lock in period of three years. Since most of us would have heard about the major differences between these two investment options, I am not going to bore you with the things you already know. This article will give you an insight of these two instruments that may give you a different perspective. I will also share my insights on which might be a better investment option for you depending on your age, risk appetite, asset allocation and more.

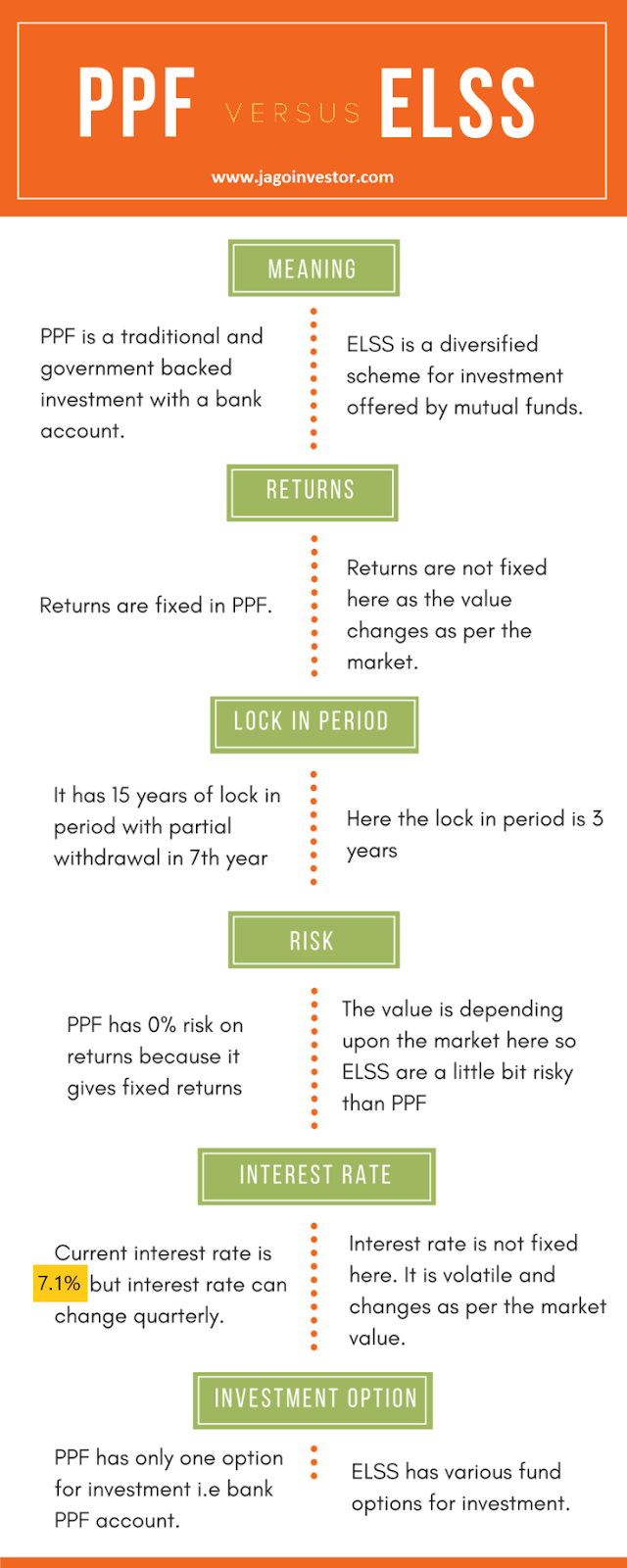

Those, who have no idea of these two instruments can get an idea from the following image:

Why is ELSS needed? Is PPF not enough?

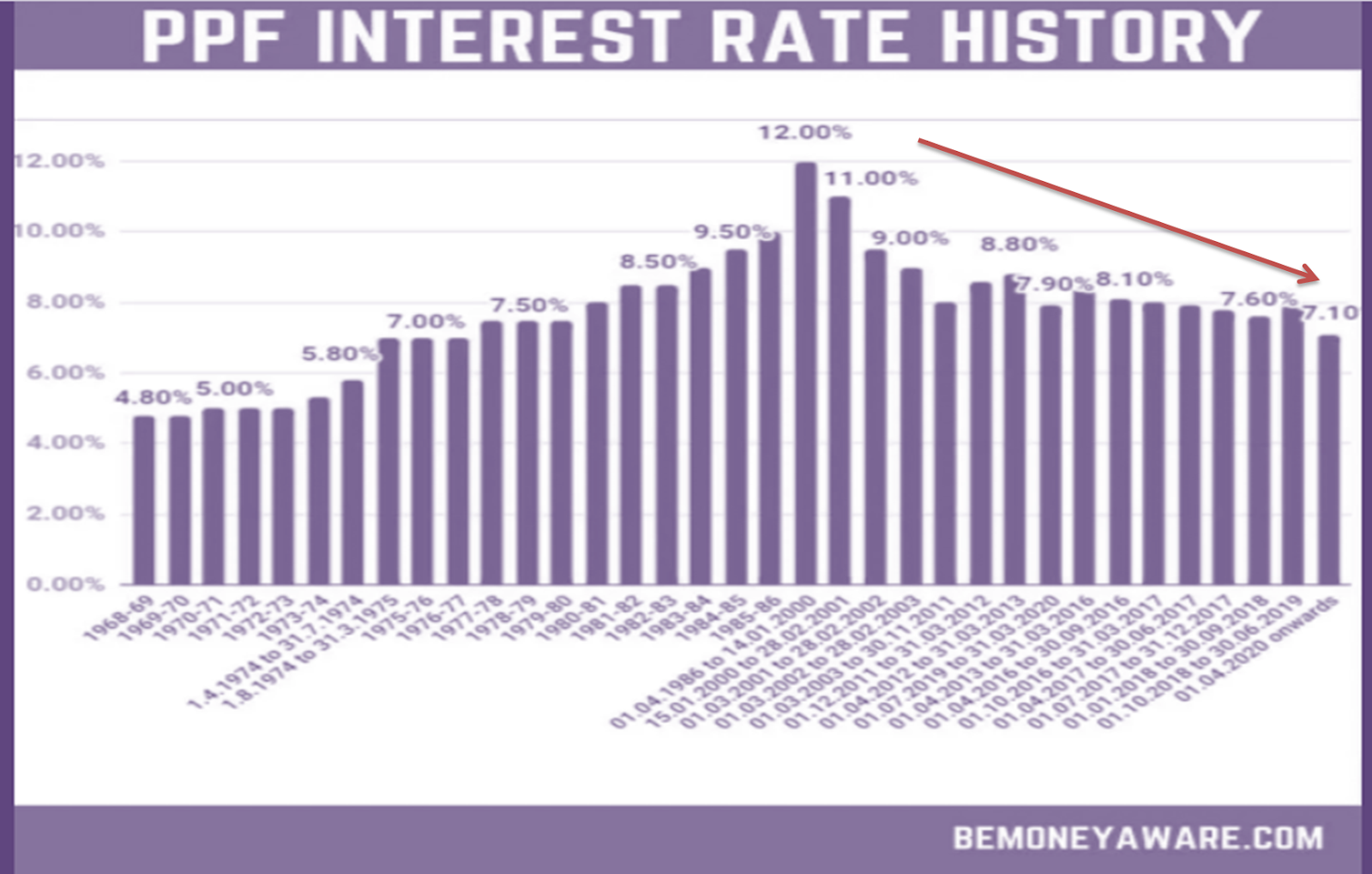

This is a common question among many of us. When PPF is giving a guaranteed return and is backed by the government, why should one consider Equity linked savings schemes which have market risks? Well, the times are changing and our economy is slowly shifting to the equity markets from the fixed investment options. The PPF returns have always been moderate and the interest rates have considerably become lower in the past twenty years. You can see this in the picture below:

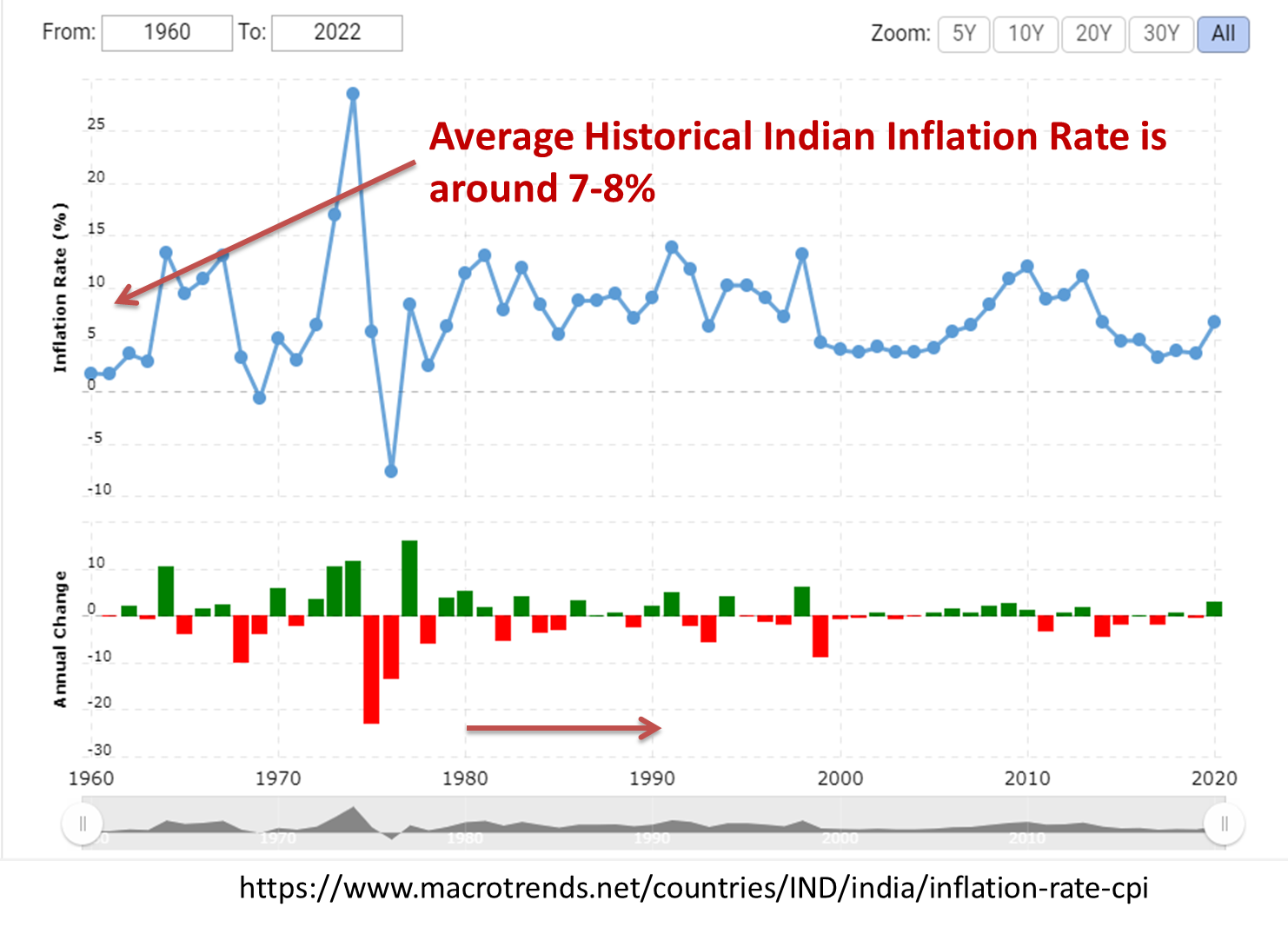

In 1986 the PPF interest rates were around 11-12%. But in the past 20 years it has decreased to just 7.1%. Though one may argue that the interest rates will fluctuate and it may go up also, that will be a rare case scenario. Even if the rates change it will fluctuate plus or minus 1%. When you are investing your hard earned money in only PPF, chances are high that your return will be just equal to the inflation rate. The historical average inflation rate of India is around 7-8% as shown in the image below:

Source : Macrotrends.net

So, when the inflation rate is around 7-8% and you get a return of 7.1% in PPF you may actually lose money or just breakeven. That is why it is always recommended not to keep large amounts of savings in Bank Fixed deposits also. So, we can see clearly that PPF alone may not be a sufficient investment option and it is better to know about ELSS mutual funds also. Nifty 50 has historically given a return of around 11% CAGR.

Comparison of Returns ELSS Vs PPF:

For comparison with PPF I have selected the following four funds:

- Axis Long term Equity Direct Growth

- Canara Robeco Equity Tax saver Direct Growth

- DSP Tax saver Direct Growth

- SBI Long Term equity Direct Growth

These funds were selected in such a way that their launch dates are almost similar. That is from 2013. Though the PPF funds are for a period of fifteen years the data analyzed here is for an approximate period of ten years only. (2013-2022). However, ten year data points would be enough for a meaningful insight. Let us see how these funds performed in the following three scenarios:

- Performance of ELSS Vs PPF in a lump sum investment

- Performance of ELSS Vs PPF in SIP Mode for the entire period

- Performance of ELSS Vs PPF in SIP Mode during market crash

ELSS Vs PPF in a Lump Sum Investment:

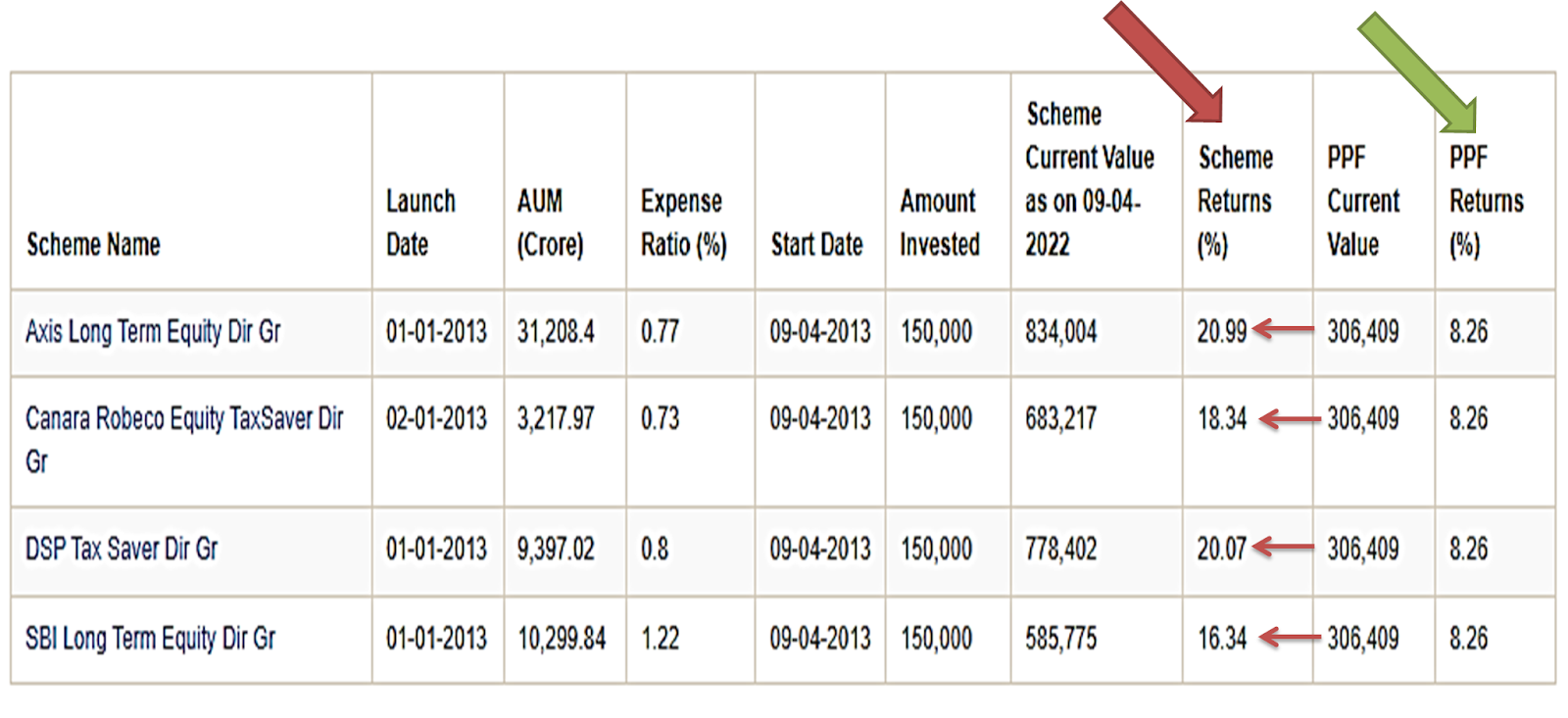

Let us assume that an investment of 1,50,000 INR is made as a lump sum investment in both PPF and these four ELSS funds on 09/04/2013. The returns as on 09 – April 2022 are as shown below:

Source : Advisorkhoj

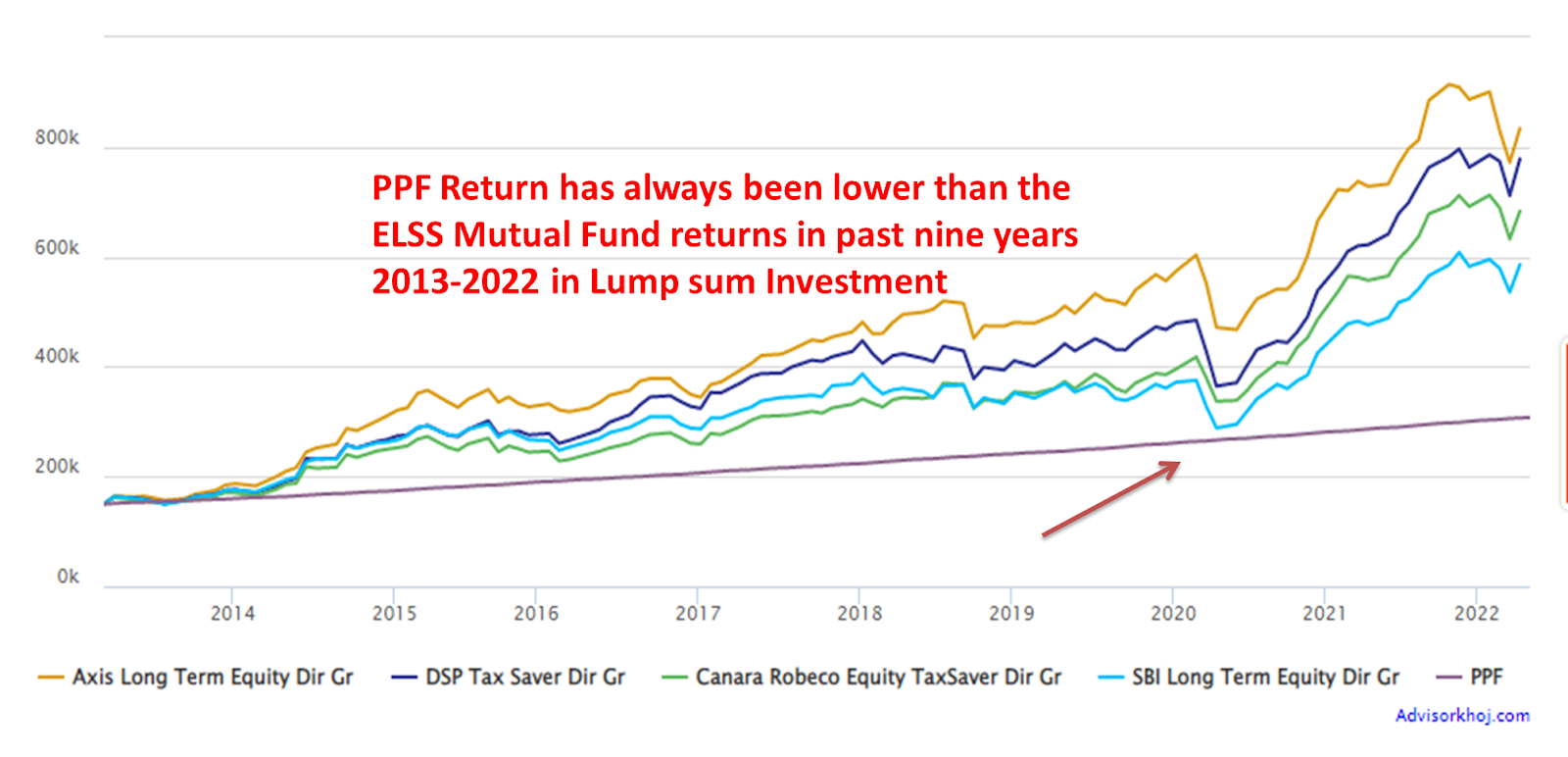

You can see that the ELSS returns have comfortably beaten the PPF returns throughout the entire period. The PPF returns are at 8.26% while the ELSS funds returns are 16-21%. Staggering outperformance. See the graph below to understand better:

All four funds have beaten the PPF returns. But, this is a hypothetical situation because no one will invest in these schemes as a Lump Sum one time investment. Even if invested as Lump sum they have to invest every year 1.5 Lakhs to gain tax benefit unlike in the above example, where 1.5 Lakhs was invested only once in the entire ten year period. This example was just to show you an idea how an ELSS has the ability to outperform PPF in the long run.

Performance of ELSS Vs PPF in SIP Mode for the entire period (2013-2022)

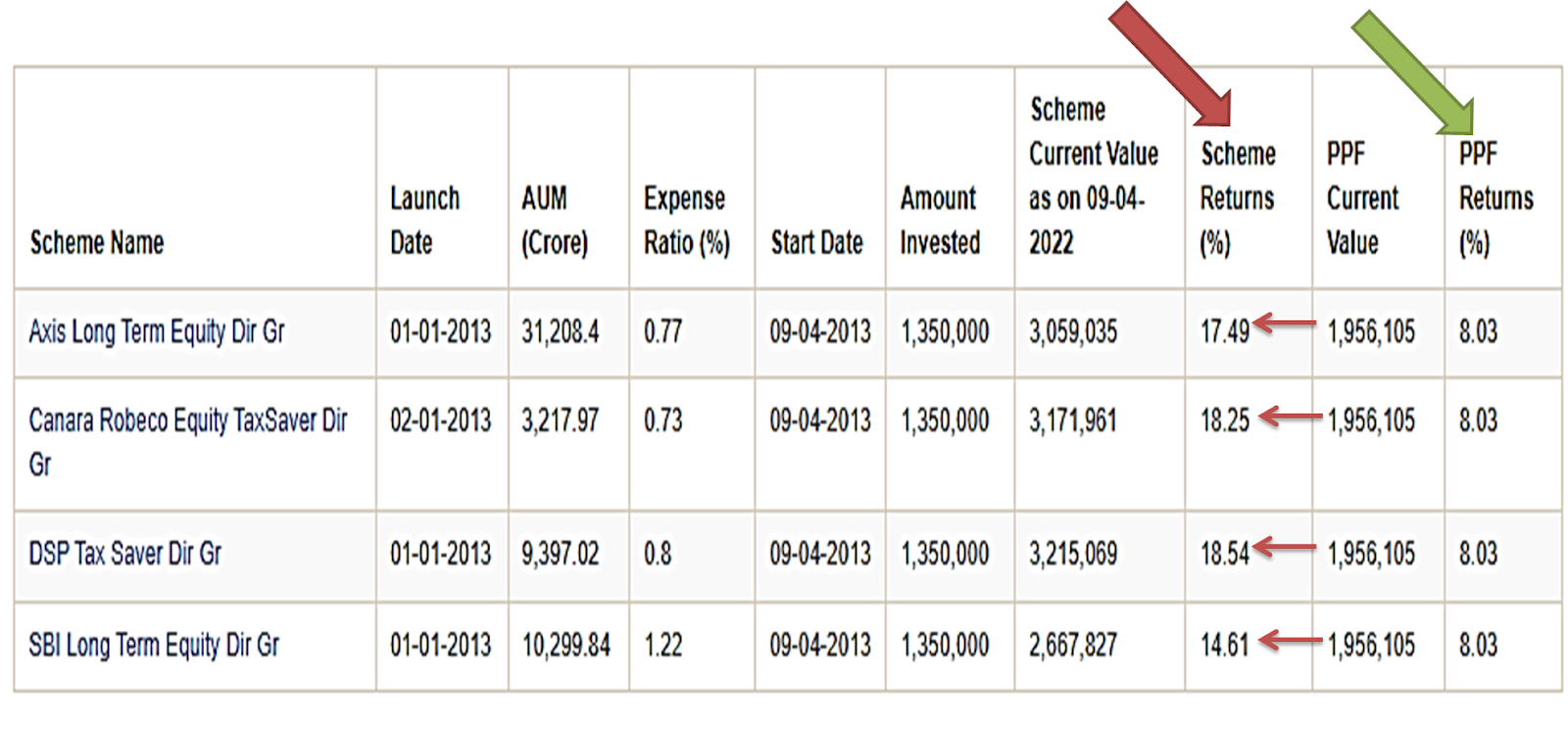

As stated earlier, it makes much more sense to compare the returns of ELSS and PPF only in SIP Mode. Let us assume that from April 2013 every month an investment of 12500 INR was made in SIP mode. The returns are as follows:

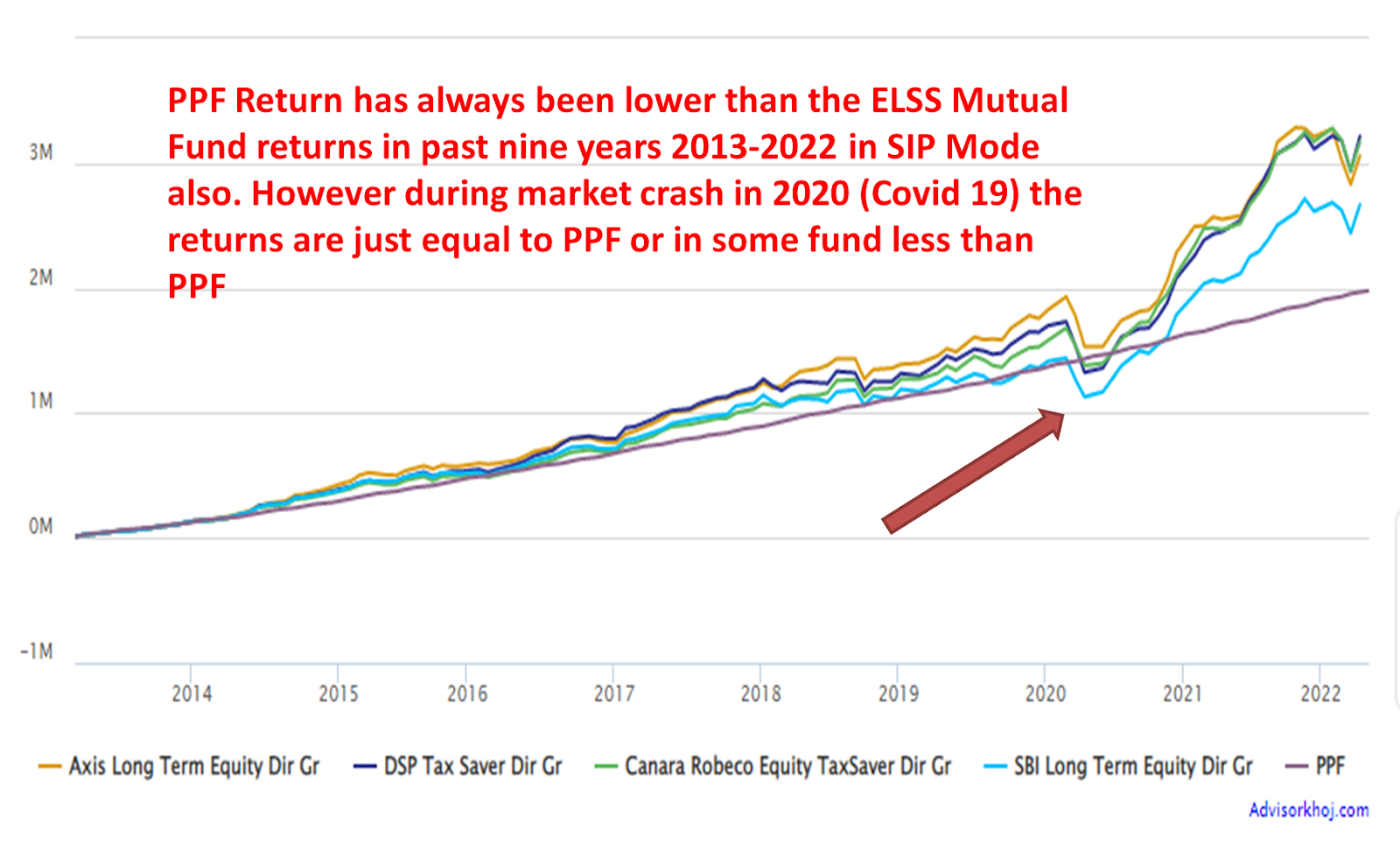

You can see the returns of the ELSS funds in red arrow and the PPF returns highlighted by green arrow. In this SIP Mode also the ELSS funds have historically beaten the PPF returns. While the PPF returns are hovering at 8.03% the ELSS Returns varies from 14.6 -17.5%. Again a great outperformance of ELSS. The returns are shown in the following graph:

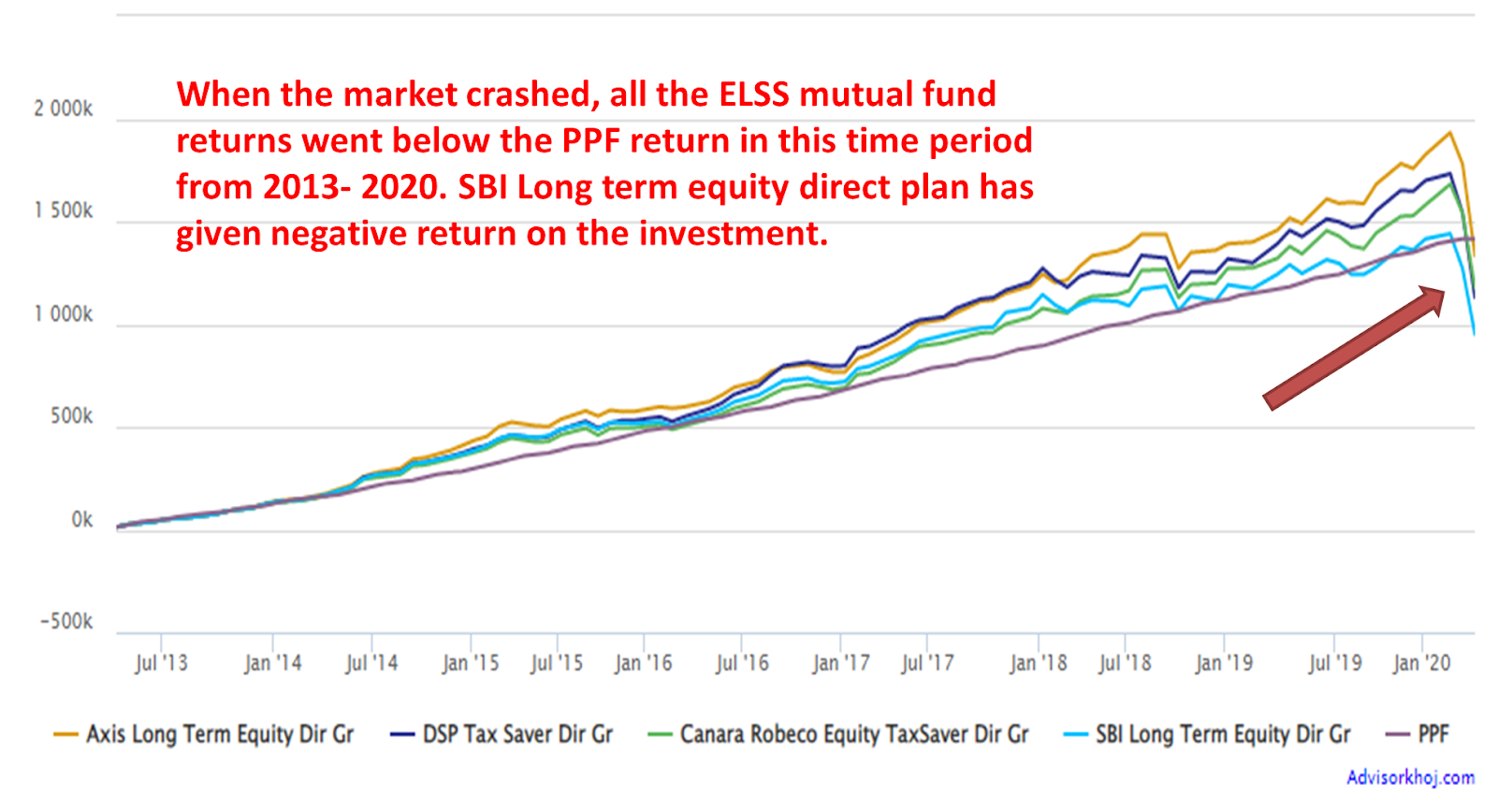

In the above graph you can see that the ELSS outperforms the PPF returns for the majority of the time period. But, during the market crash due to Covid 19 pandemic the returns have just dropped equal to that of PPF in Axis fund and in other funds even lower than PPF (Shown in red arrow).

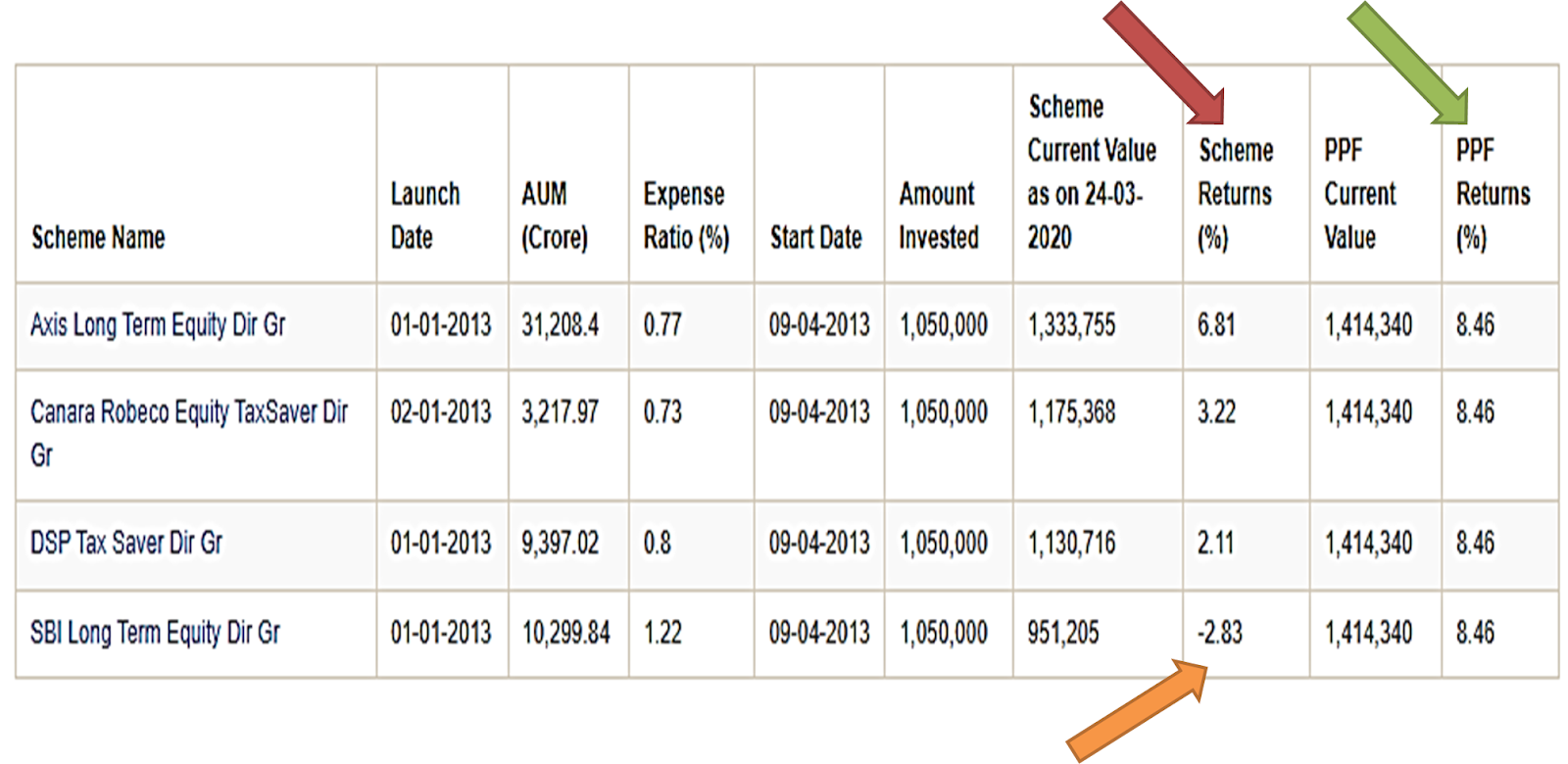

Performance of ELSS Vs PPF in SIP Mode during market crash :

Capital preservation is very important for a retail investor. Capital appreciation comes second. So it is wise to see how these funds’ returns were on the day of March 24 -2020 when the index crashed and touched its low due to the pandemic. The results are shown below:

You can see that the PPF returns are at 8.46% while none of the funds were able to beat the PPF returns from 2013-2020. In fact SBI fund has given the worst performance with a negative return on the investment of -2.83% (orange arrow) and the best performance is the Axis fund with 6.81% (lower than PPF).

Note: Don’t think that SBI mutual Fund is a bad fund just by seeing this result. It could have happened to any fund. To decide whether a fund is good or bad we have to do more research and see the consistency of the fund’s performance and rolling returns which I will discuss in a separate article.

The specific date was taken just to give an insight of what would have been the return of ELSS if the lock-in period ends on March 24-2020? ELSS are often advertised as an all time success. It gives a misconception that the ELSS returns will always beat the PPF returns. While it may be true for most of the times, it is also possible to get a negative return or a return equal to or lower to PPF.

In the above scenario, how would you manage? Will you panic and withdraw all the amount in one go or will you wait? Because historically whenever the market crashes, usually it bounces back within a year or so. If you are able to manage without redeeming your ELSS within a year, the returns would have been massive. However, if you have planned to use this money for something else like your son / daughter education needs, marriage or any other urgency that could not be postponed, you would be forced to withdraw the amount from ELSS as you don’t have the luxury to wait for some more years. This is why asset allocation is very important and you should be prepared for these surprises in your investment journey.

What is best for me? How to choose?

Though it is not possible for me to decide which is best for you, I can give you some insights on how you can decide.

Define your Goal:

First and foremost assess your goal for the amount you save in these Tax saving schemes.

Without having a proper goal everything can go wrong. You should be clear in mind what you are going to do with this money at the end of the fifteenth year or maturity period. For what you need this money? Is this a part of your retirement corpus or is this going to be used for your son / daughter education or marriage?

You may wonder why it matters. See, if you are planning this as a retirement corpus you can take that extra risk to invest more in ELSS than PPF. Because even if the ELSS Returns are poor or negative as we saw during the market crash (2020) you can wait a year or two before withdrawing. Thereby you can give some time for the market to correct.

But, suppose if you have planned this money for your children’s education or marriage or any other important thing that cannot be postponed, you will be forced to withdraw the money even if the returns are not as expected. In that case, it would have been better to invest more in PPF than ELSS.

Your Age at the time of starting Investment:

If you have started your investing journey early in your career, the ability to take risks will be easier. An investor who starts investing from the age of 25 will have a different risk profile compared to an individual who starts late at 35-40 years of age. So, if you are an early investor you can definitely go for ELSS so that you can wait a few more years to redeem, even if the returns are poor at the end of maturity period.

Retirement Age:

Have you planned your retirement age? If you are 40 and you had planned to retire by the age of 55 then the period for your retirement is 15 years. If your retirement corpus is dependent upon this corpus kindly avoid investing more in ELSS as the returns are not guaranteed. Alternatively, if you are 30 years of age and you plan to retire by 55 years then you have 25 years of time for retirement. As the time to retirement increases the ability to take risks becomes easier. So, you can invest more in ELSS than PPF.

Asset Allocation:

Another important aspect to consider is how much money you have allocated for equities and Fixed income like debt mutual funds / Fixed deposits etc., in your portfolio. Suppose your portfolio is 20 Lakhs worth and you have already allocated 70% (14 Lakhs) of it in equity and you plan to continue to do so then adding ELSS again may result in increased equity exposure. So, plan your asset allocation and then consider which is good for you. If you cannot decide on your own you can surely get in touch with a fee only financial advisors.

Alternative Ideas:

You can also choose to invest 50% in PPF and 50% in ELSS. If you are investing 10,000 as monthly SIP for tax saving purpose you can invest 5000 INR in PPF and another 5000 in ELSS.

Or you can follow asset allocation strategy also here. You can invest 70% that is 7000 INR in the ELSS equity scheme and the remaining 3000 in PPF.

By doing these kinds of combinations you will be able to enjoy the benefits of both worlds and your risk is also reduced to a larger extent. At the time of maturity, say fifteen years, if the ELSS fund has not given you the return you expected due to some market underperformance, you can redeem the PPF amount and use it for the purpose intended. After a year or so when the market recovers you can slowly withdraw the amount from ELSS schemes.

Another method is to invest in ELSS for the first 8-9 years and then from 10th year to 15th year you can start investing in PPF. If you are planning to start investing in a Tax scheme from this year (2022), for the next fifteen years and plan to redeem the amount in 2037 then, till 2032 you can invest in ELSS and the next five years you can invest in PPF. But remember that you have to start the PPF account also at the same time you start ELSS investment. This is because you can’t just start a PPF in 2032 and withdraw in 2037 (15 years lock in period). So, start both accounts at the same time, but invest just 500 every year in PPF (minimum transaction needed to keep the account active).

The advantage of this is equity schemes have always given a positive return in the long run and as you go closer to the maturity period, you start investing in PPF thereby reducing the risk to a greater extent.

Key Takeaways:

- With the interest rate of PPF is on a constant decline, it is expected to decline further. This makes it mandatory for us to think of equity related tax saving schemes to beat inflation in the long run.

- ELSS has given outperforming results compared to PPF, but it is possible to get a return that is lower than PPF return in case of a market crash.

- Investing in both ELSS and PPF in a 50-50 or a 70-30 allocation can give good returns with reduced risk.

- More than all, set a clear goal plan of what you are going to do with the invested money and for what you are investing that money.

- If you are still confused feel free to consult your financial advisor.

- Happy investing!!!

One thought on “PPF Vs ELSS – A COMPARATIVE ANALYSIS (Find out which is best for you?)”